SpaceX - Thesis & Valuation Memorandum

Probabilistic sum-of-the-parts valuation | Q2 2026 | Pre-IPO

Executive Summary

SpaceX is the most important company of this century as its combined ambitions address the largest TAM of any company in history, far beyond the S1 estimation of 28.5T. SpaceX is growing at an unprecedented rate for a trillion-dollar tech conglomerate and is rapidly converging an array of highly synergistic businesses in its quest to make consciousness multi-planetary, deliver superior connectivity infrastructure and accelerate mankind via a maximally truth-seeking generalized artificial intelligence. Dialectic herein posits a near-term valuation target of $179/share (blended equity value $2.405T) with a long-term valuation target (10yr+) of 10T. Our first-principles, scenario-weighted, sum-of-the-parts DCF across the estimated twelve business units produces a P50 enterprise value of $166/share ($2.241 trillion), with meaningful right-skew to $352/share $4.733 trillion at P90. We will continue to accumulate SPCX up to our P55 of $179/share, continue opportunistically adding via proprietary strategies up to our P75 of $258/share and favour holding while employing our advanced yielding strategies on top of the asset there above until more information becomes clear. Our probabilistic sum of the parts DCF is complemented by a comparables analysis that considers a moderate ‘Elon Premium’ against peers, as well as current market signals.

We note that there is considerable upside potential from this base given the dominant market position in the various emerging markets that are tangential to space exploration, AI, and connectivity. We observe accelerating network effects across the approximately twelve (12) business lines currently operated under the SpaceX brand. While this document does not contemplate a pending highly strategic and synergistic merger with Tesla, we do note additional upside potential therein. At Dialectic, one of our principles is that ‘the future is far more Sci-Fi than you think’. SpaceX is pulling mankind towards a literal Sci-Fi future, more than any other company on the planet (or off planet) and we consider exposure to this asset fundamental for our future-forward investment portfolio.

Investment Thesis

SpaceX is rapidly accelerating its strategic advantages across the different business units in the primary categories 3 categories of 1- Space exploration, 2- connectivity, and 3- AI + Digital, with special consideration to the synergistic convergence of these businesses and resultant network effects.

Pillar 1: Space -- Network Effects & Moat in Access to Orbit

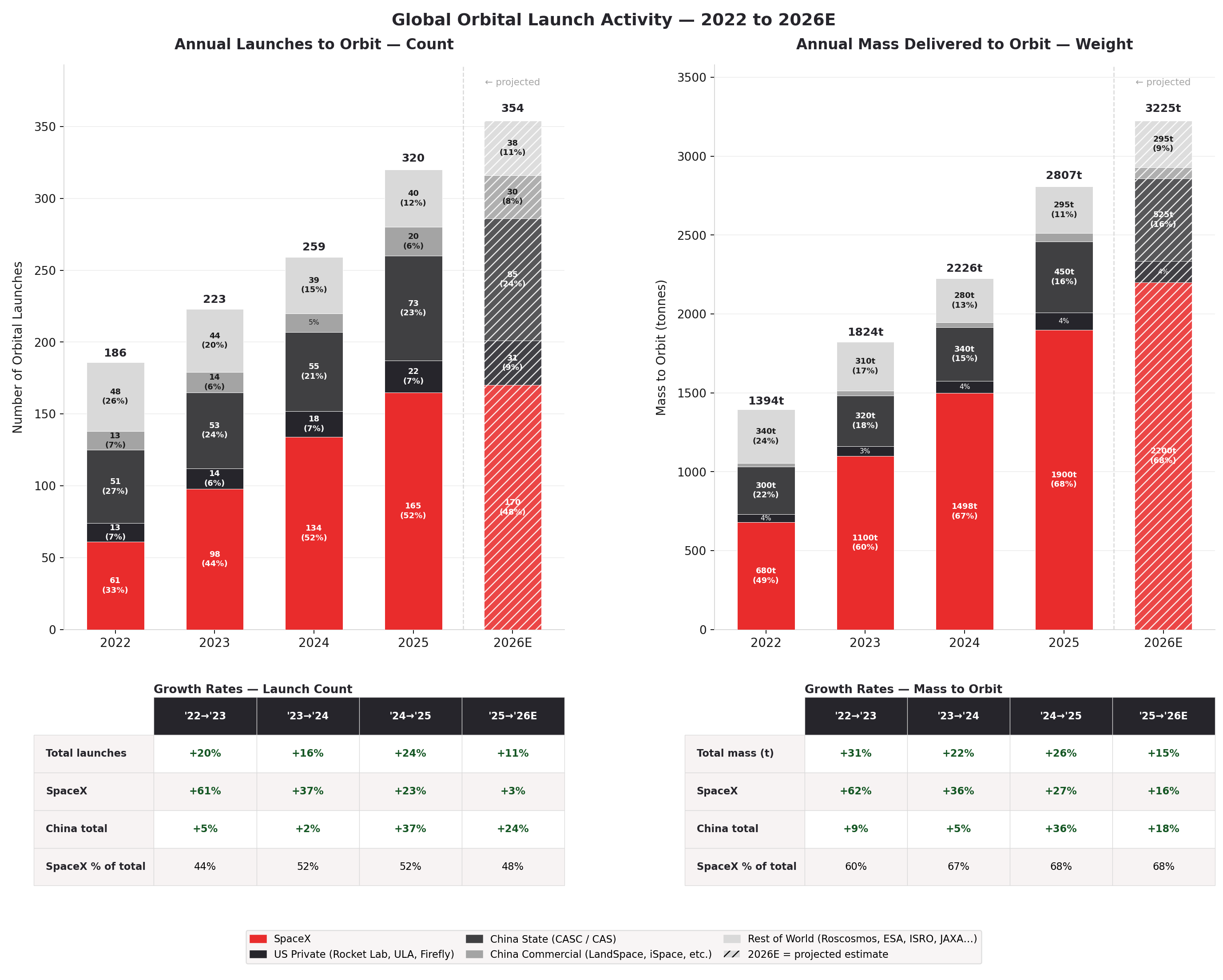

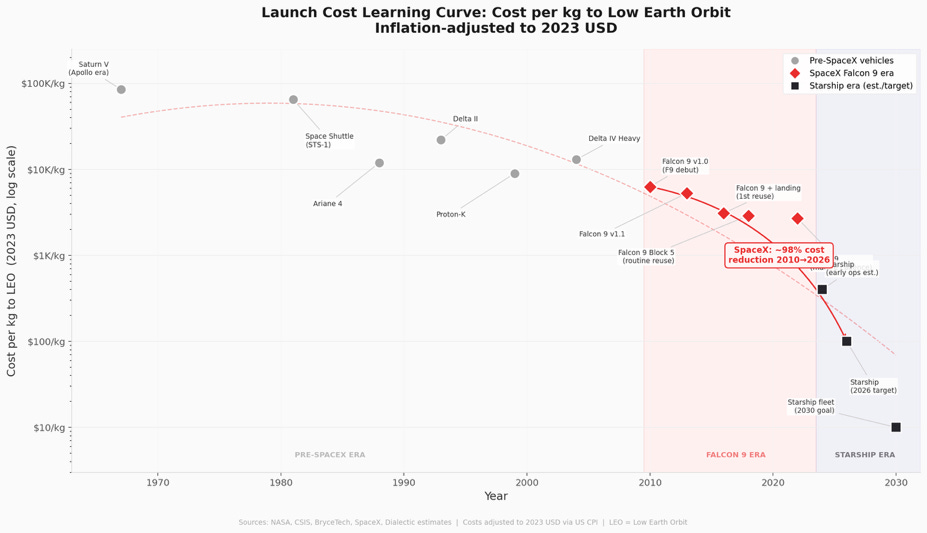

SpaceX has fundamentally repriced access to orbit, reducing commercial launch costs by over 90% since Falcon 9’s introduction. With 140-145 Falcon 9 launches expected in 2026 and Starship approaching commercial readiness in the later part of the year, SpaceX holds an incredibly advantageous competitive position and accounts for a significant majority of all launches globally by count and by weight-to-orbit. No competitor can match SpaceX on cadence, reliability, and price as Starship’s sheer scale drops the cost-to-orbit below $100/kg, driving under $10/kg by 2030. We are witnessing the SpaceX transcend Wright’s Law and push us towards a Space Age version of Moore’s Law. A fully operational Starship opens a $150B+ cargo-as-a-service near-term TAM.

Pillar 2: Connectivity -- Starlink as a Global Telecom & Internet Infra + D2C

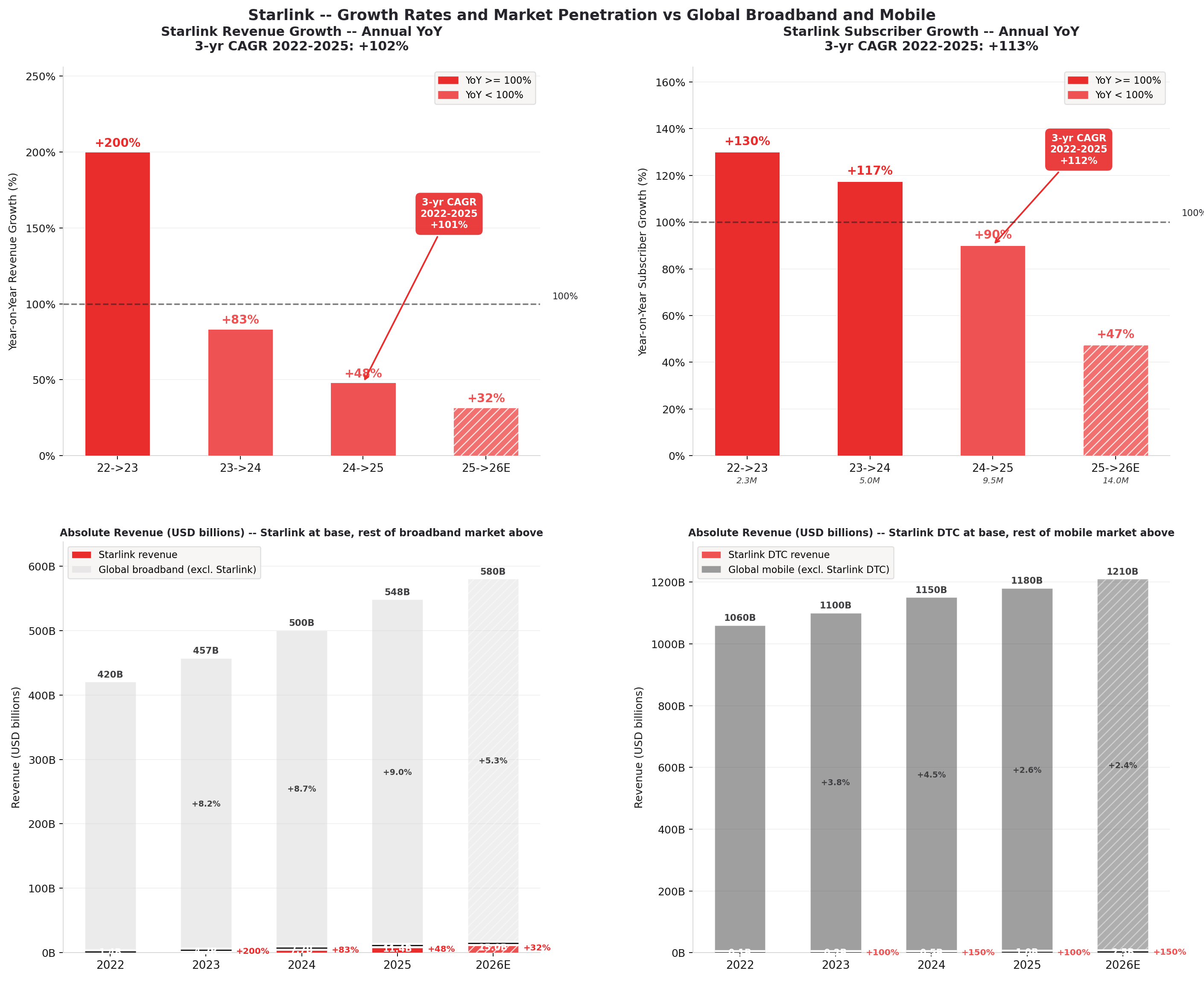

Starlink is not just a satellite internet company. It is a global telecommunications network that will pass terrestrial communications infrastructure in cost, reliability and eventually latency/performance. It is an internet infrastructure business with recurring subscription-based revenue, low marginal cost per additional subscriber, and structural advantages over every terrestrial and geostationary competitor. At 12+ million subscribers across 164 countries and growing over 100% annual CAGR, Starlink generates $11.4 billion of annual revenue with a 63% EBITDA margin. Direct-to-Cell extends the Starlink franchise to mobile devices globally and should capture some of the approximately $400 billion in cellular telecom annual profits.

Pillar 3: Maximally Truth-seeking AI -- The AI Infrastructure Stack

The winner in AI Foundation Models - which we often refer to within Dialectic as “the Sport of Kings” (Bill Gurley, 2024) for its extraordinary capex vs TAM dynamic - will be decided on 3 fronts: 1- Data, 2- Compute, and 3- Algorithmic innovations. The 2025 merger with xAI created a unique vertically integrated AI company: the only entity that simultaneously trains frontier AI models (Grok), operates its own GPU cluster at unprecedented scale and speed of execution (Colossus), distributes models to 600+ million users (X.com) which generates exclusive proprietary training data and financial transactions (Xmoney), while building orbital compute infrastructure supported by fabrication of semiconductor chips for both terrestrial edge-nodes and orbital training, all connected via its own global communications network.

An important but misunderstood advantage of Grok/xAI is the principle to develop a maximally truth-seeking AI -- this allows Grok to learn and develop at a different pace than models that have an ideological throttle placed on them. A maximally truth-seeking AI also builds deep trust with users and will ultimately deliver superior performance in recursive learning environments.

Colossus I recently closed $26 billion in agreements with Anthropic and Google demonstrating significant growth potential of Colossus in the short term, while SpaceX prepares for the future of Orbital Data Centers.

Pillar 4 -- The Convergence Flywheel

It will become more obvious over time that the true value of SpaceX is not merely the sum of its parts -- it is their synergistic intersection and resultant growth. SpaceX manufactures satellites, launches them on its own rockets, and produces the full global connectivity stack, connecting with its own manufactured edge-nodes with Tesla robots and potential internally developed edge-node devices. X’s 600M+ users generate exclusive training data for Grok, a maximally truth-seeking AI. XMoney (launched April 2026 with Visa integration across 41 US states) monetizes those interactions with embedded fintech. Starshield and Golden Dome contracts ($6.45 billion awarded in 2026 alone) leverage the same orbital expertise built for Starlink as the defining ‘defense neo-prime’ in a time of significant geopolitical uncertainty. ODCs present medium-term advantages with respect to energy, cooling, networking, and permitting. These businesses support off-planet resource extraction, manufacturing and eventually interplanetary colonization. We often ask ourselves, ‘what is the TAM of the boundless potential of space?’. Every business unit strengthens every other and is unified under a singularly ambitious mission and common culture often referred to “as a zone of shocking competence” (Marc Andreesen, 2026), where the pace of work and growth is unmatched globally.

Business Unit Analysis

SpaceX is a somewhat complex conglomerate operating across a range of current and near-term. For the sake of simplicity in this first iteration of our analysis, we have divided the business into 12 segments, worked through revenue and profitability potential on 3 different horizons, while heavily weighting near-term potential for the sake of conservatism. By some internal accounts SpaceX is actually more than two dozen different businesses and we built up revenue projections by looking at each one from first principles, using public sources. We expect public figures to become more widely known post the 2026-Q2 reporting and intend to update this analysis as new information becomes available. This is an incredibly dynamic business.

1 -- Launch Services

The Orbital launch segment generated $4.086 billion of revenue in FY2025 at roughly $653 million of adjusted EBITDA — a ~16% margin that has been depressed during the Starship development cycle. SpaceX accounts for roughly 85% of all global satellite launches, having repriced access to orbit; we expect 140-150 Falcon 9 launches this year at roughly $74 million per launch. Our model update revises the 2026 base revenue to $11.5 billion. The bull case requires some Starship commercial revenue to materialize in 2026-2027. Given competitor challenges in recent months, this seems. We accounted for lower EBITDA margins in the near term by Starship R&D (~$15B). As Starship becomes operational and the development drag rolls off, margins should converge toward 40-50%. Our scenarios apply revenue CAGRs of roughly 15% / 25% / 45% (Bear / Base / Bull), and S-1 calibration lifted our base-case revenue anchor from ~$6.8B to ~$13.5B as the HLS Artemis lunar-lander and Starship cadence ramp.

2 -- Crewed Trips, 3 -- Other Space Services

NASA CCP/CRS and deposits received for manned private spaceflight make up current revenues. NASA crewed missions account for $700M-$900M of annual revenue inside of this decade, supplemented by Polaris and Axiom private-astronaut missions. There are distinct plans for private spaceflight, both interplanetary and globally (global point-to-point in less than 45 minutes via Starport infrastructure) that could be significant as well. Other space services — satellite servicing, orbit-to-orbit transport (orbital tug), and rocketry IP licensing or manufacture for sale — are a smaller line modeled conservatively but capable of opening entirely new business lines. These segments are also where SpaceX’s Mars ambitions begin to monetize: as the cadence and payload economics improve, the path toward a self-sustaining off-planet presence underwrites optionality that the comps cannot capture. Elon has referenced a space hotel in a recent JP Morgan roadshow appearance. Overall, we have these segments as relatively benign in the scenario weighting, but we maintain them as a placeholder as there is outlier potential for these segments over time, particularly as the core mission of SpaceX (and Elon’s compensation) are centered around a threshold of inhabitants on Mars.

4 -- Starlink Connectivity

Starlink is SpaceX’s cash cow: $11.39B revenue and roughly $7.17B of adjusted EBITDA in 2025, a 63% margin that expanded from ~50% as the constellation scaled and fixed costs leveraged. 12M+ subscribers across 164 countries. ARPU compressed from $86 to $66 as Starlink expanded into lower-income geographies, but the May 2026 price increase signals a deliberate shift from land-grab toward monetizing the existing base. Aviation and maritime adoption are rapidly accelerating and carries materially higher ARPU than the consumer tier. S-1 calibration lifted our base-case revenue anchor from ~$9.8B to ~$18B, and our scenarios apply revenue CAGRs of roughly 15% / 35% / 55% (Bear / Base / Bull) with margins trending toward the mid-60s.

5 -- Starlink Direct-to-Cell

DTC represents an entirely new revenue stream, monetized initially through carrier licensing fees from T-Mobile, KDDI, Optus, Rogers and others. The addressable opportunity is large — global cellular profits run ~$400B/yr, and the directly serviceable supplemental-coverage market is on the order of $40-100B — of which Starlink should be able to capture a significant component. Crucially, Direct-to-cell rides on the Gen2 constellation, which is already launching, so the marginal cost of per additional client is relatively low. Bilateral spectrum agreements now exist in dozens of countries. This is the most binary segment in the model on a 5-year basis: outcomes hinge on spectrum, handset compatibility, regulatory/political questions, and carrier deal-structure rather than on technical feasibility - which is now demonstrated. With the new generation of Starlink satellites offering superior speeds, we could very well see massive adoption growth in home and businesses as Starlink goes from internet back-up or remote use-cases to core home and business internet connection.

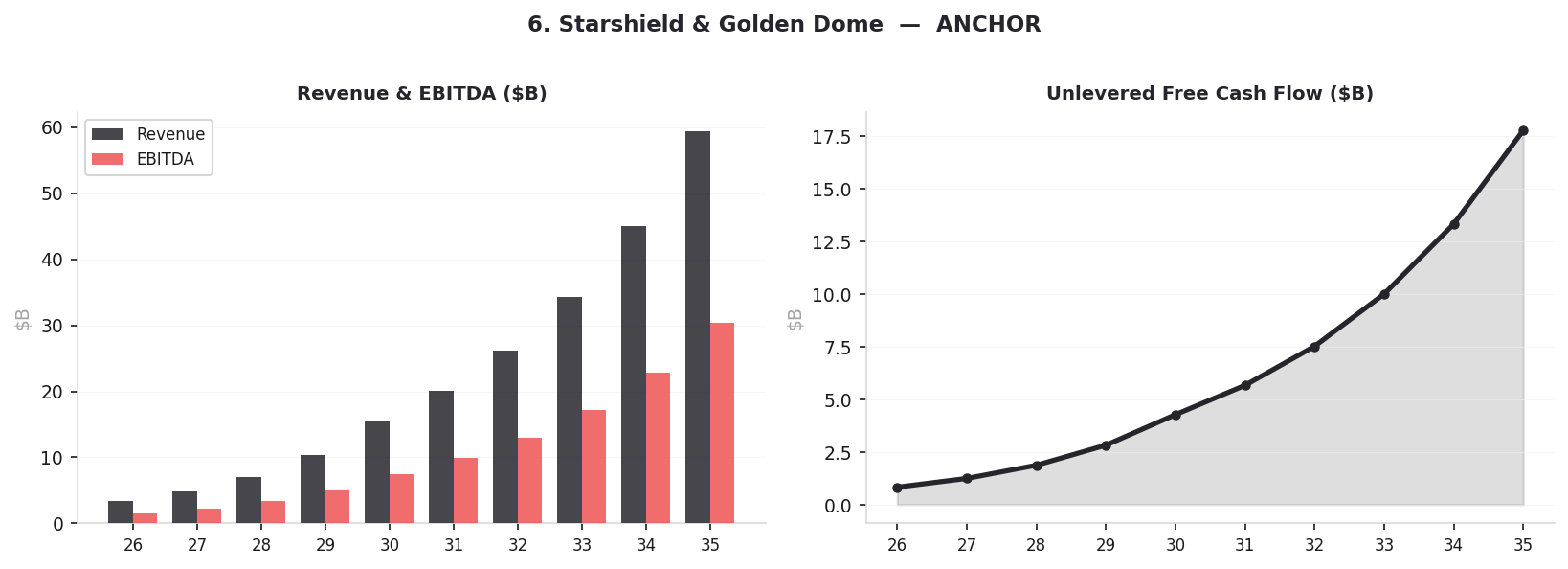

6 -- Starshield & Golden Dome

SpaceX is the best-positioned defense neo-prime contractor in an era of considerable geopolitical uncertainty. $6.45B in new Golden Dome contracts in 2026: the SDN Backbone at $2.29B (with an end-2027 prototype milestone) plus AMTI satellites at $4.16B. Additional awards: an NRO $1.8B classified satellite contract and a Space Force PLEO IDIQ ceiling of $13B. In aggregate, SpaceX’s recent defense awards exceed the combined awards of all other companies in the segment, underscoring its leading neo-prime status. These contracts are multi-year, so initial revenues are conservatively projected with lower weighting; our scenarios run a base case near $2.3B scaling toward a bull case of roughly $6.5B as Golden Dome and Starshield production ramp.

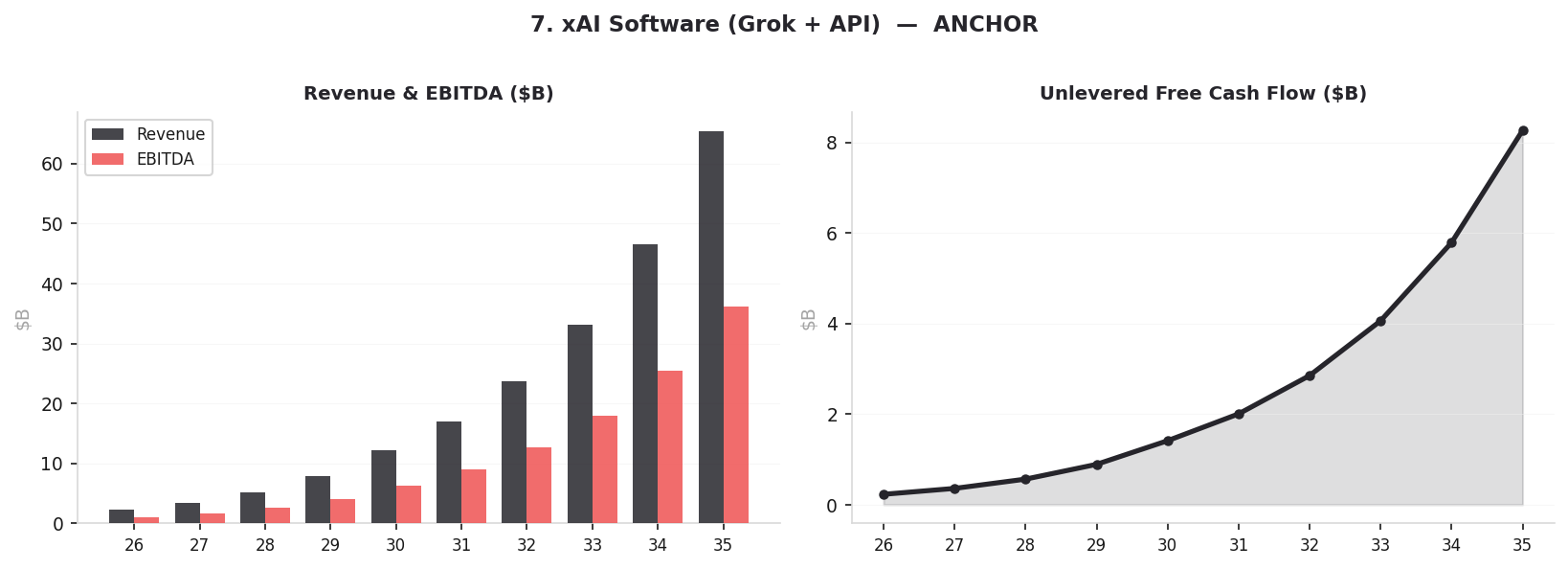

7 -- xAI Software (Grok + API)

Grok + API $3.201B of revenue in FY2025 against an operating loss of roughly $(6.355B) — the heavy training-and-talent investment that funds Grok’s position among the top two-to-three frontier models. The application layer is inflecting fast: Cursor went from $1B in ARR in November to $2B+ in ARR in March, and we assume the ~$60B acquisition is likely to consummate shortly after the IPO. Monetization runs across SuperGrok, enterprise API, and rapidly growing DoD / Department-of-War contracts, with X distribution (600M+ users) providing a low-cost-CAC funnel. AI Foundation models, or “the Sport of Kings” is an incredibly competitive and capital-intensive indusrty and thus the AI business is currently unprofitable. We expect inflection to profitability by late 2026 into early 2027 as inference costs fall and enterprise/API revenue scales against a largely fixed base. Also, Macrohard could prove very compelling and Grok Build is rapidly scaling, entering an era of recursive self-improvement and asymptotic intelligence.

8 -- Colossus Terrestrial Data Centers

The 300MW, 220,000 NVIDIA GPU-equivalent cluster in Memphis — stood up in a now-famous 122-day build that demonstrated SpaceX/xAI’s shocking speed advantage in deploying compute. The $15 billion Anthropic and $11 billion Google agreements validate the market-clearing price for frontier GPU-hours and their resultant tokens, and these contrasts de-risk the buildout by underwriting third-party demand alongside xAI’s own training needs. SpaceX targets roughly 1 million GPU-equivalent additions per year, a commitment it intends to sustain across a multi-year horizon. Colossus II is now operational, training novel Grok models, Macrohard, and it serves as the terrestrial bridge to the Orbital Data Center roadmap.

9 -- X Platform & XMoney

550-600M MAU and roughly 245-250M DAU, with $3.5B of FY2025 revenue of which ~70-75% is advertising — a base that has recovered strongly from the ~$2.7B 2023 trough. XMoney launched April 2026 with Visa integration, P2P payments across 41 US states, >100M DAU on the payments surface, and 6% APY on deposits. Our model raises X Platform’s 2026 base revenue to $7B, reflecting XMoney, creator monetization, AI-targeted advertising powered by Grok, and an expanding app scope toward the WeChat-style super-app model — a transition that, if it lands, drives non-linear revenue per user rather than the linear ad-load economics the current multiple assumes.

10 -- Orbital Data Centers

In-space compute with distinct advantage – lowered levelized cost of energy with high capacity-factor solar arrays, improved cooling through highly engineered radiators, faster networking via lasers through the vacuum of space, and the elimination of the NIMBY/permitting constraint (holding up nearly 50% of planned US data centers). This business line is conservatively classified as speculative; estimated first commercial operation in 2030, noting that there is a reasonable chance that ODCs come online before that and have significant upside similar to Colossus or are potentially delayed in achieving scale. The transformational case is cost-per-FLOP parity with terrestrial compute: once orbital launch and on-orbit assembly costs fall far enough that a watt of space-based compute is competitive with a watt on the ground, the structural advantages above (energy, cooling, networking, no permitting) convert a niche into a potential platform shift in where large-scale AI training is done — a market SpaceX is uniquely positioned to serve given its launch, satellite, and chip-fabrication stack.

11 -- Deep Space Optionality

Deep Space Optionality includes a range of far-reaching businesses that are on the roadmap, but possess economic models that are not as well understood — Lunar then Mars colonization, resource extraction on other planets and asteroids, orbit-to-orbit transport, and exploratory R&D. We note that ambitious targets, such as 2028 lunar missions, sustain a narrative premium and attracts the best talent in aerospace. Our model treats this as a small probability-weighted DCF contribution that we treat as a deep-DCF, so it does not double-count optionality recognized elsewhere.

12 -- Terafab

The vertically integrated semiconductor fabrication project announced in March 2026 building 1- custom space-optimized ASICs for training in space, 2- high-performance compute for Colussus, and 3- specific edge-node inference chips both for Tesla robots and cars alongside a potential edge- node device with telecommunications (think, the next generation of the smart phone) that SpaceX is uniquely positioned to offer. The world’s largest chip-manufacturing facility under one roof, and the most vertically integrated: Terafab is designed to consolidate chip design, lithography, HBM memory, advanced packaging, and test under a single roof — the steps that today are fragmented across TSMC, ASML, SK Hynix and others. It would supply SpaceX’s own roadmap (AI5-class FSD silicon, AI6-class Optimus inference, and D3-class space-hardened training chips) rather than depend on the merchant market. Target capacity is over 1 terawatt of AI compute per year. First phase is ~$55B, with full buildout up to $119B. Revenue is modeled beginning 2031 to account for the unknown unknowns in chip design and foundry development, making this the longest-dated and most heavily discounted line in the SOTP.

Valuation Analysis

Methodology

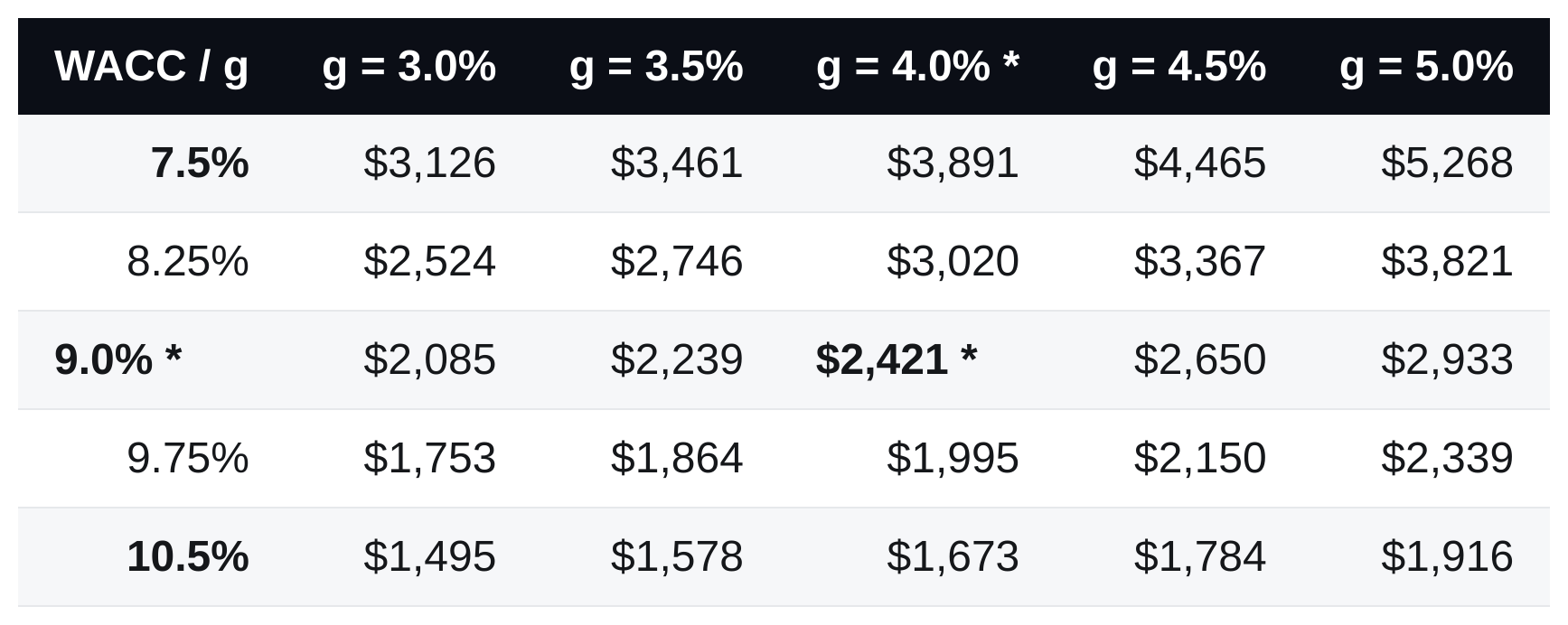

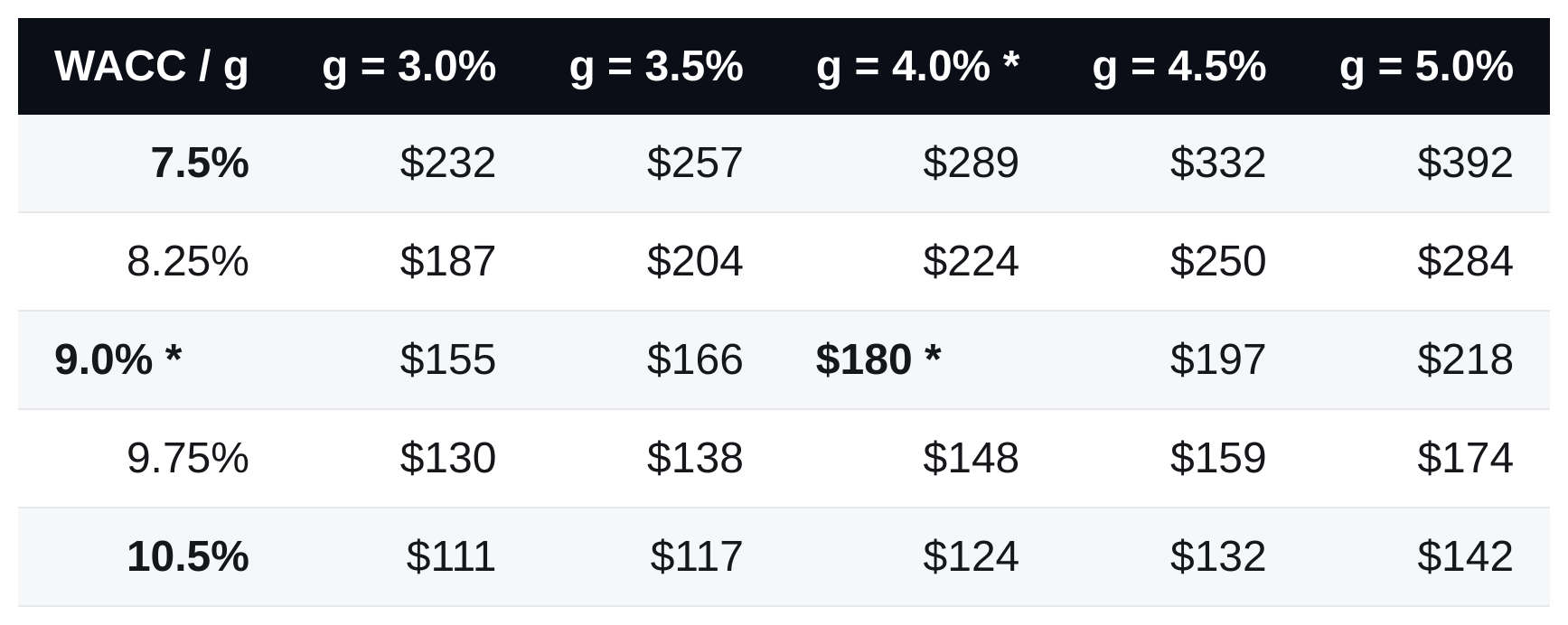

We primarily employed a bottoms-up, probability-weighted sum-of-the-parts (SOTP) DCF across twelve business units, each modeled with three scenarios (Bear / Base / Bull) and a materialization probability considered in short, medium and long time horizons with strong overweighting near-term cash flows. The DCF tab discounts the resulting UFCF at a blended WACC of 9.0% with a terminal growth rate of 4.0%. In addition to this valuation model, we evaluate comparables in relevant industries and consider the Elon Premium alongside Current Market Signals.

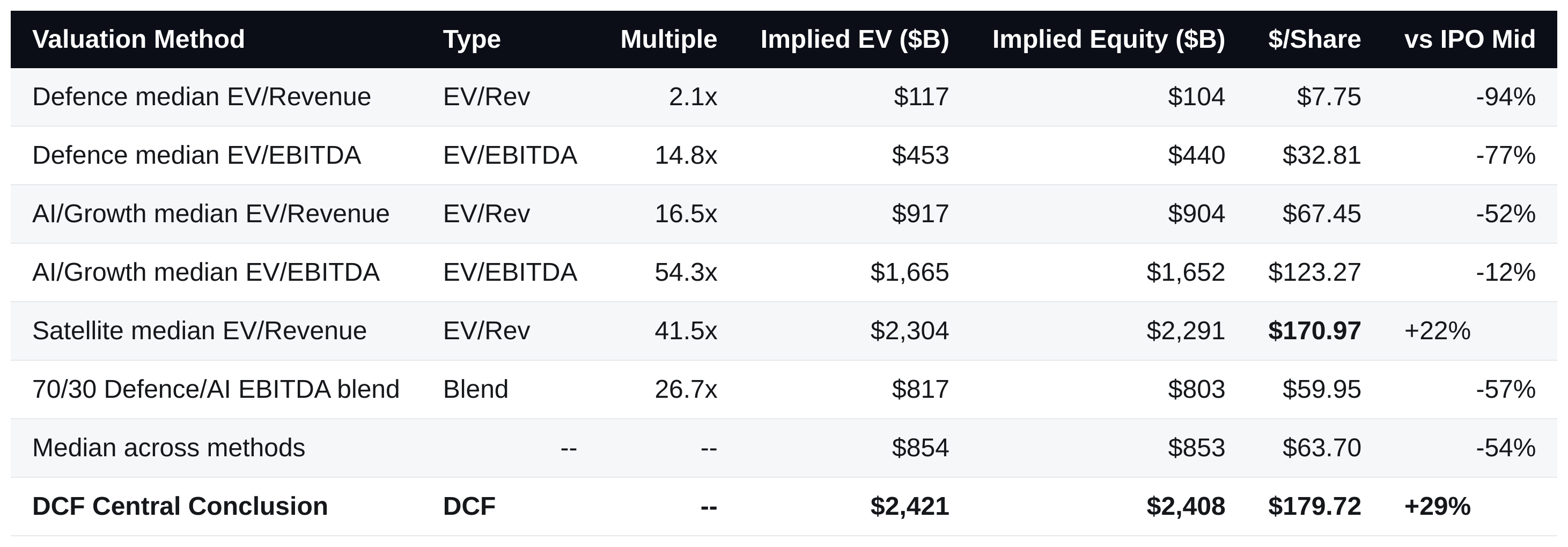

Comparables Analysis

We treat trading comparables as a cross-check and a downside bound, not as the primary basis for value. SpaceX has no clean peer. A blended whole-company multiple is therefore directional at best, which is why our central value rests on the sum-of-the-parts DCF.

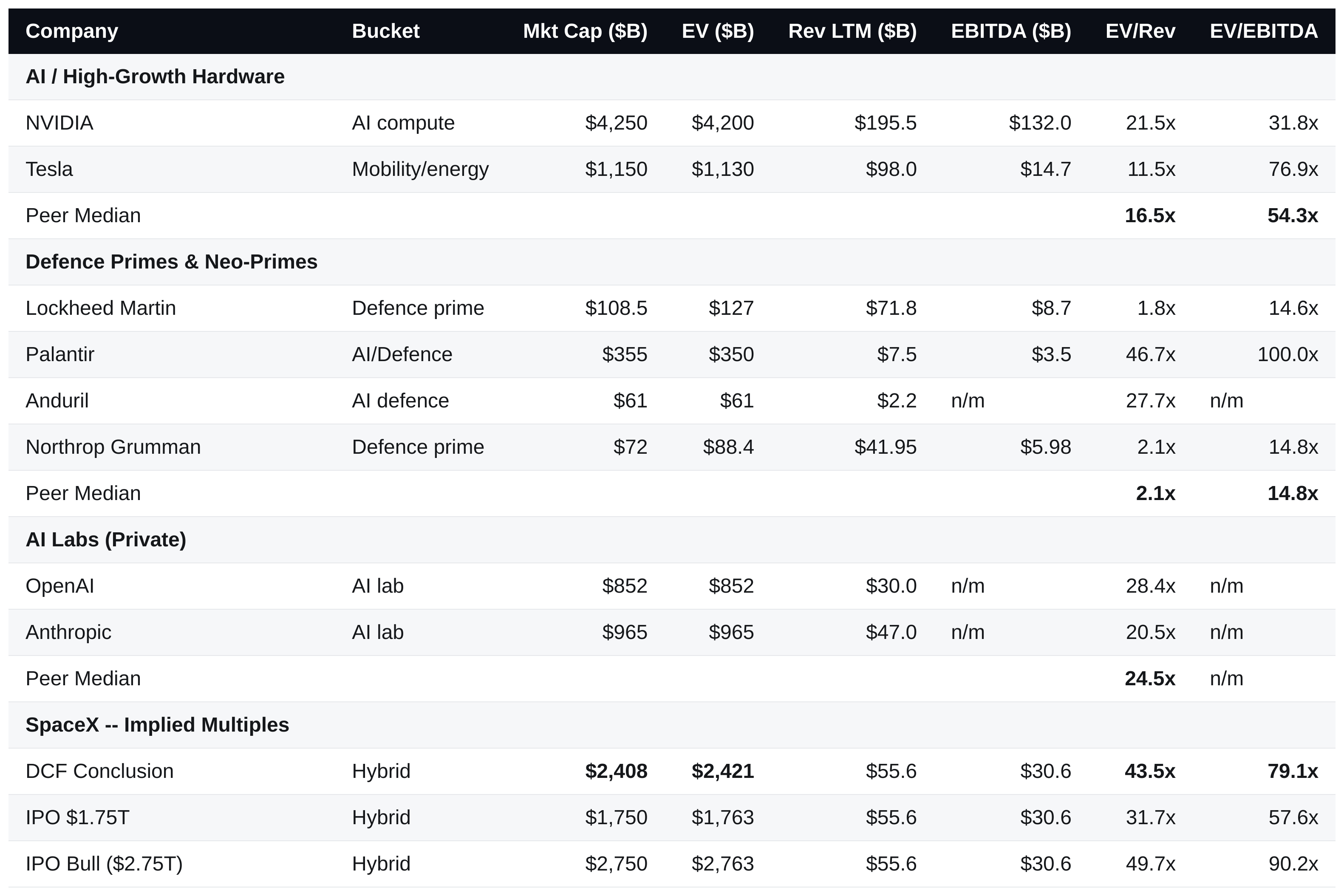

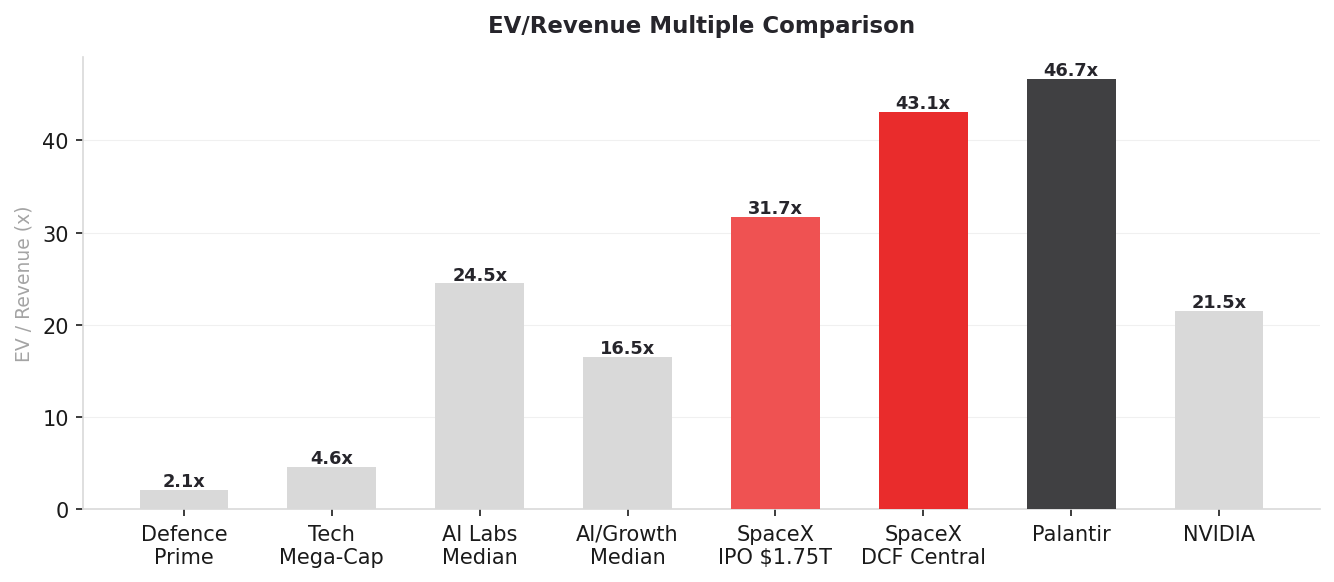

Viewed across the relevant peer sets, the comparables span an extremely wide band. Defense primes trade at roughly 2x revenue and anchor low, while high-growth satellite and new space names (Rocket Lab, AST SpaceMobile) trade at multiples that, applied to SpaceX’s revenue base, would imply values up to ~$2.47 trillion. The AI cohort sits between these poles: OpenAI screens at roughly 28x Revenue and Anthropic at roughly 21x, Palantir — the closest listed AI/defense neo-prime analogue — at roughly 47x Revenues, alongside NVIDIA at roughly 22x. Applying the AI and high-growth multiples to SpaceX’s revenue implies an equity value in the $1.0-1.7 trillion zone, broadly consistent with the DCF.

The synthesis is that comparables price the company as it is today, not the convergence flywheel we underwrite, and they penalize SpaceX for being mid-cycle in a heavy-investment phase. They are therefore most useful as a soft floor — framing value near $0.9-1.0 trillion — with the DCF and the IPO range describing where the market is actually likely to clear, given the Elon Premium.

Elon Premium

Across peer groups, SpaceX valuation implies an average Elon Premium of roughly 1.8x against the AI-lab median of OpenAI and Anthropic (24.5x EV/Revenue), while being in line with Palantir, the closest listed AI/defence neo-prime comparable at 46.7x EV/Revenue vs SpaceX’s 43.5x EV/Revenue and 79.1x EV/EBITDA (2026E, DCF conclusion) to frame the premium. On EBITDA, the picture inverts the headline: SpaceX screens roughly 80% Palantir’s 100.0x, i.e. the one preferred peer that is profitable. OpenAI and Anthropic carry no EBITDA multiple as both remain pre-EBITDA. Surprisingly, our valuation has SpaceX at the same revenue multiple as space industry peers despite extraordinary structural advantages.

The Elon Premium is best understood as compensation for the compounding optionality of an operator who moves faster, builds more ambitiously and competently, and controls more of the value chain than any single peer. SpaceX has no clean comparable.

Current Market Signals

Hyperliquid and Polymarket have been pricing the enterprise valuation between $2.17 and $2.45T for the last several weeks with $42M and $2.3M in daily volume respectively, which substantiates the legitimate market depth of these positions.

Risks & Key Considerations

Execution & Technology Risk: Starship’s commercial timeline is a risk, as is the timeline of direct-to-cell, Terafab and to a lesser extent Colossus, and Starshield. Numerous projects, in particular Terafab, represent enormous capital commitments with binary outcomes. If the $55 billion Terafab Capex does not produce cost-competitive chips for AI training, it could be written down.

Key-Man Risk: All of the businesses are dependent on Elon Musk for design direction and important cultural leadership. Any event that reduces Musk’s involvement -- legal, political, or personal -- would likely cause rapid multiple compression, even if the risk event doesn’t affect business fundamentals or competitive positioning.

Regulatory & Political Concentration Risk: SpaceX’s Starshield and Golden Dome revenues are politically concentrated in the current administration. Particularly, an antagonistic Democrat-controlled branch of government could hold back the business in different ways. A change in administration could materially slow or cancel government programs. Other countries and companies could decide not to work with SpaceX for geopolitical reasons, thereby propping up the competition and digesting some market potential over time. Regulatory risk is also the primary concern with respect to a potential merger with Tesla.

Competition & Market Structure: Our analysis concluded that the most significant competition across the business units of SpaceX comes primarily from China today, both from state-sponsored projects as well as private enterprises such as i-Space and LandSpace. It would be unwise to underestimate the Chinese in their ability to develop, manufacture, and push the boundaries of exploration. Space pure-play competitors in America do exist and are growing with formidable backing – Amazon’s Blue Origin, Rocket Lab ($RKLB), and Eric Schmidt’s Relativity are all relevant, even amidst some technical setbacks and scale limitations therein.

Note: We observe with opportunistic excitement the flowering of an array of ‘SpaceX Cubs’ or ‘SpaceX Mafia’ – offspring led by former SpaceX team members that are building compelling technologies. Impulse, Verda, Apex, Firefly and others may present new opportunities for acquisition and these different experiments may prove positive.

Finally, but very importantly, the cost of serving intelligence in AI is rapidly decreasing, which could have profound impacts on society and industry. The nature of AI may fundamentally change to primarily edge-computing, open-source. Recursive learning could result in totally unforeseen solutions to the compute dirth. There are many ways AI could commodify quickly, rendering massive previous capital expenditure as sunk cost.

Financial & Balance Sheet Risk: Total long-term debt of $29.1 billion against cash of $15.9 billion produces net debt of $13.2 billion. Q1 2026 burned $8.9 billion in cash (R&D and xAI integration costs). The $75 billion IPO raise is indeed necessary for short term growth. Further dilutive fundraising could drag down return profile in the short and medium term.

The Elon Premium: The Elon Premium is real, measurable, and -- in our view -- historically justified. SpaceX at 43x 2026E Revenue requires the market to continue believing in the full convergence flywheel and for multiple business units to have successful outcomes. Note that at $1.5 trillion ($112/share), the Elon Premium comes for free.

Conclusion

When we look up towards the stars we are reminded of the infinite possibilities of space and the inspiring Sci-Fi future that mankind will chart as a multi-planetary species. SpaceX is uniquely positioned as the most consequential private company of the 21st century, potentially in the history of capitalism. The flywheel of vertical integration across these businesses is compounding in ways that no competitor can replicate. At 43.5x 26E Revenues ($55.6B) and our DCF blended fair value of $179/share ($2.418T), we reiterate our conviction on the accumulation plan set herein. The opportune issuance of SPCX may be remembered as the most extraordinary gift to America on the eve of her 250th Anniversary. At current levels the investor buys the current business across launch, connectivity, AI and digital. The Moon, Mars and potentially many other celestial bodies are free, as is the impact of a maximally truth-seeking generalized intelligence as recursive self-improvement takes hold.

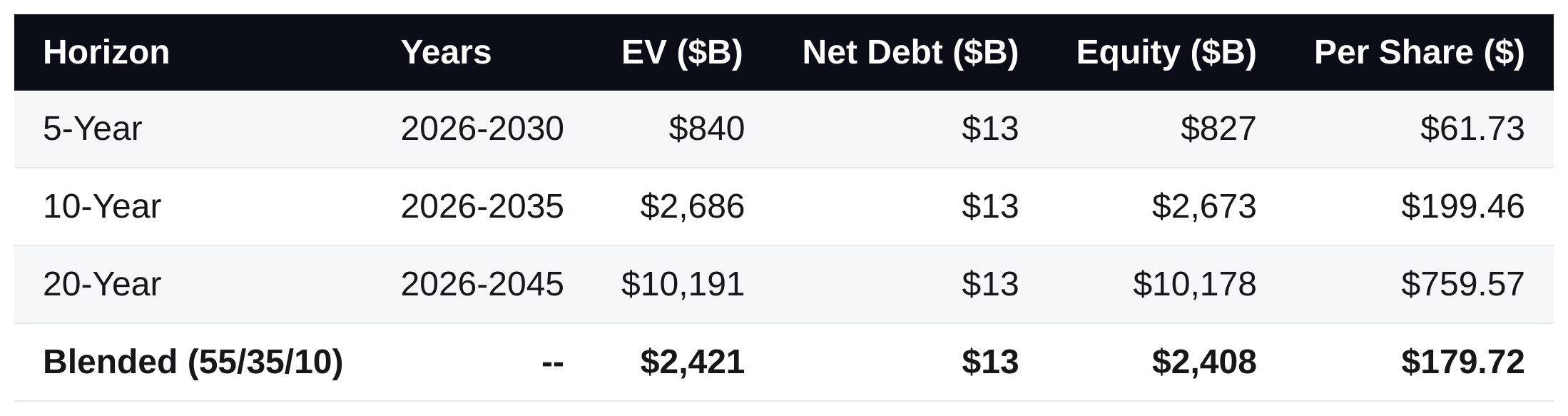

ANNEX A | PROBABILITY-WEIGHTED VALUATION SUMMARY

A

Probability-Weighted Valuation Summary

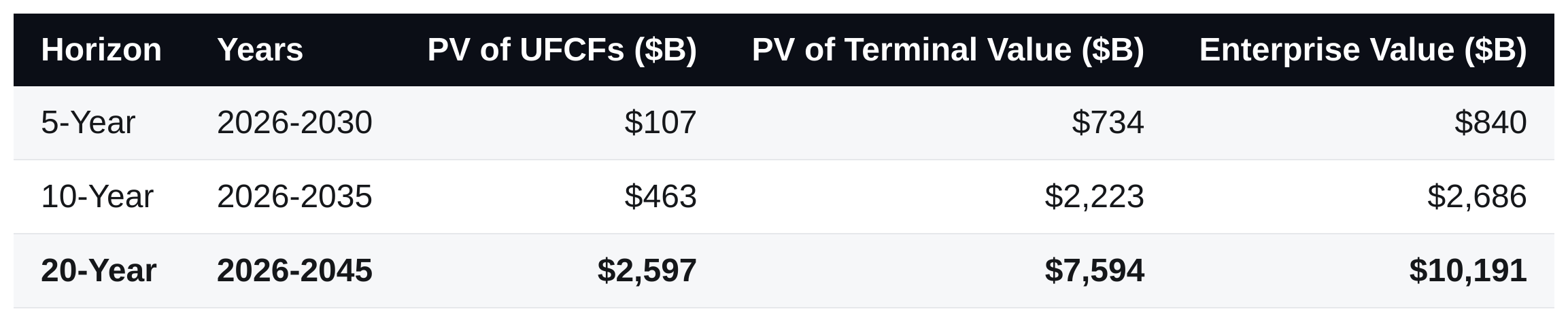

Blended EV, equity value, and per-share across 5yr, 10yr, and 20yr horizons. WACC 9.0%, terminal g 4.0%, net debt $13.3B, 13,400M diluted shares.

Blended weights: 5yr 55%, 10yr 35%, 20yr 10%. Horizon weights set by investment committee to reflect near-term certainty premium.

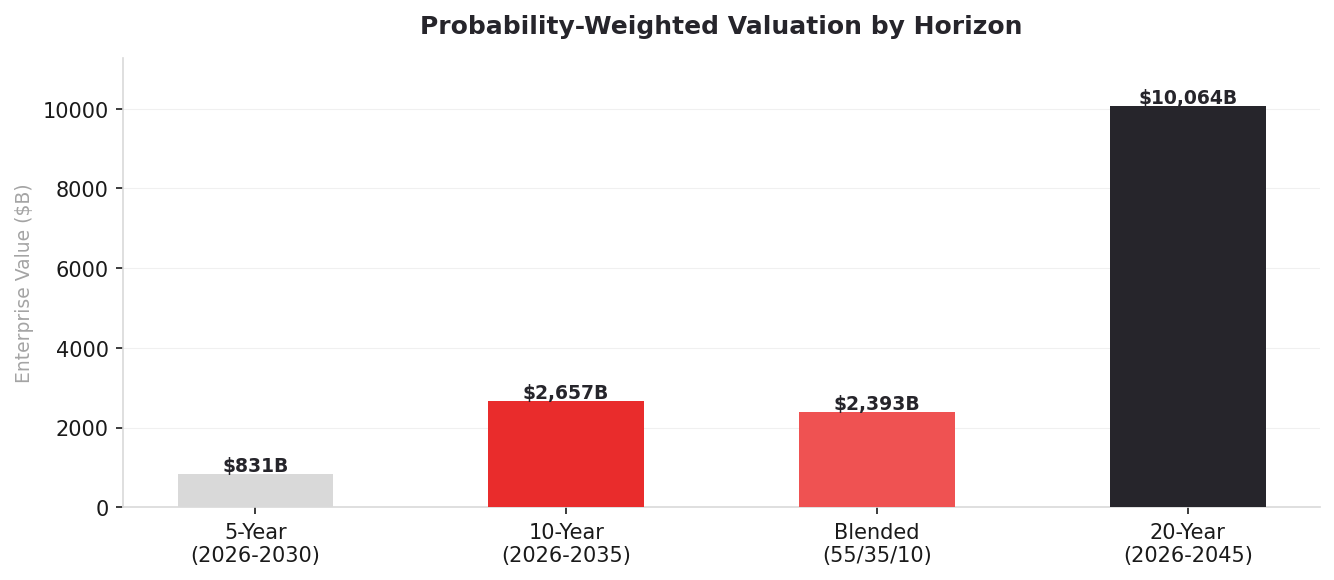

Figure A1: Enterprise value by horizon. Blended (55/35/10 weighted) = $2,421B.

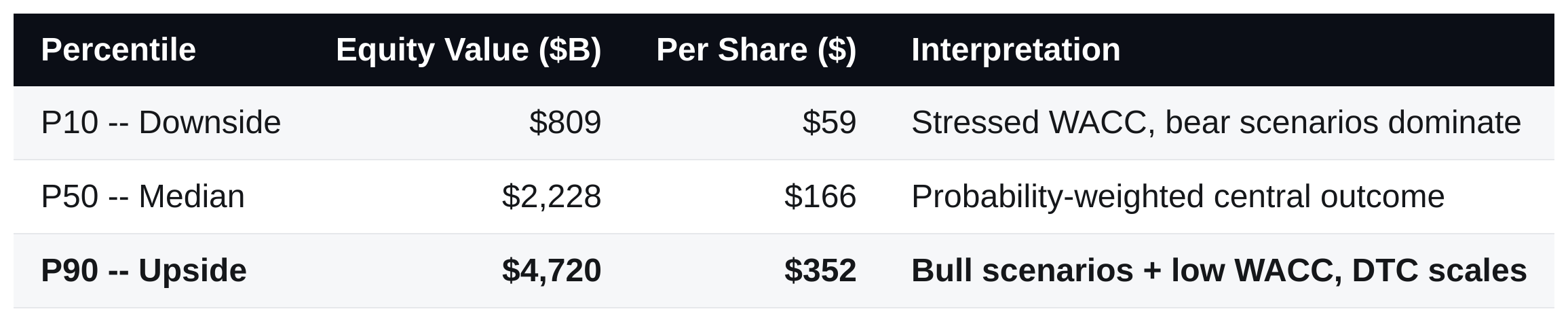

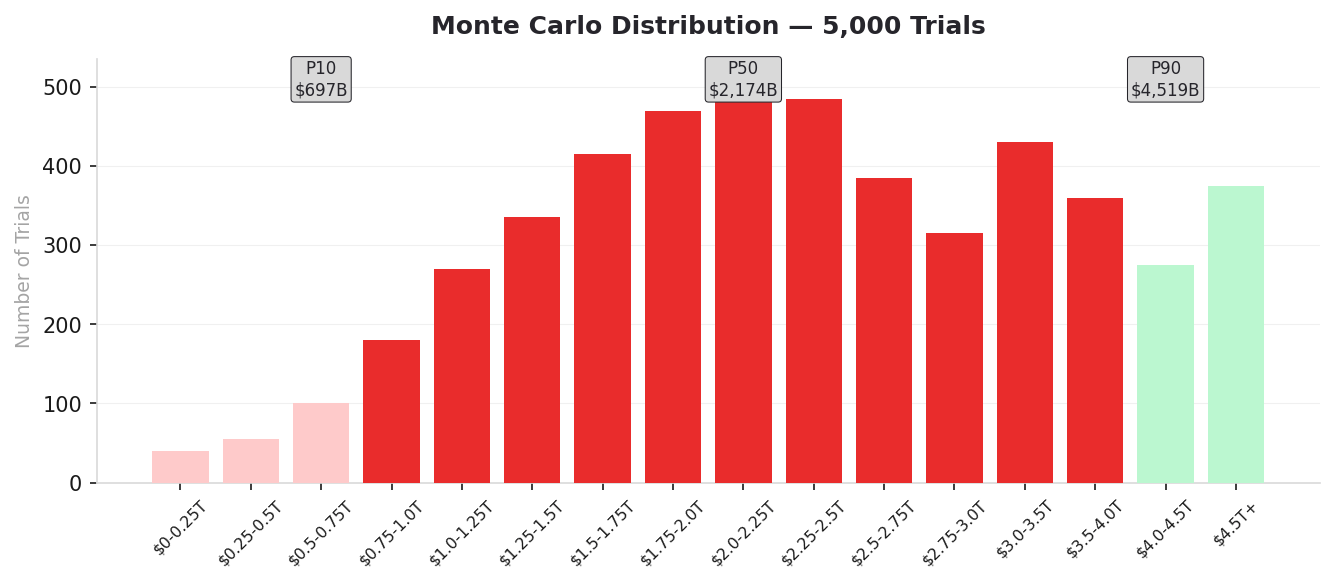

Monte Carlo Distribution (5,000 Trials)

Figure A2: Monte Carlo equity distribution. P10 shaded red, P90 shaded green.

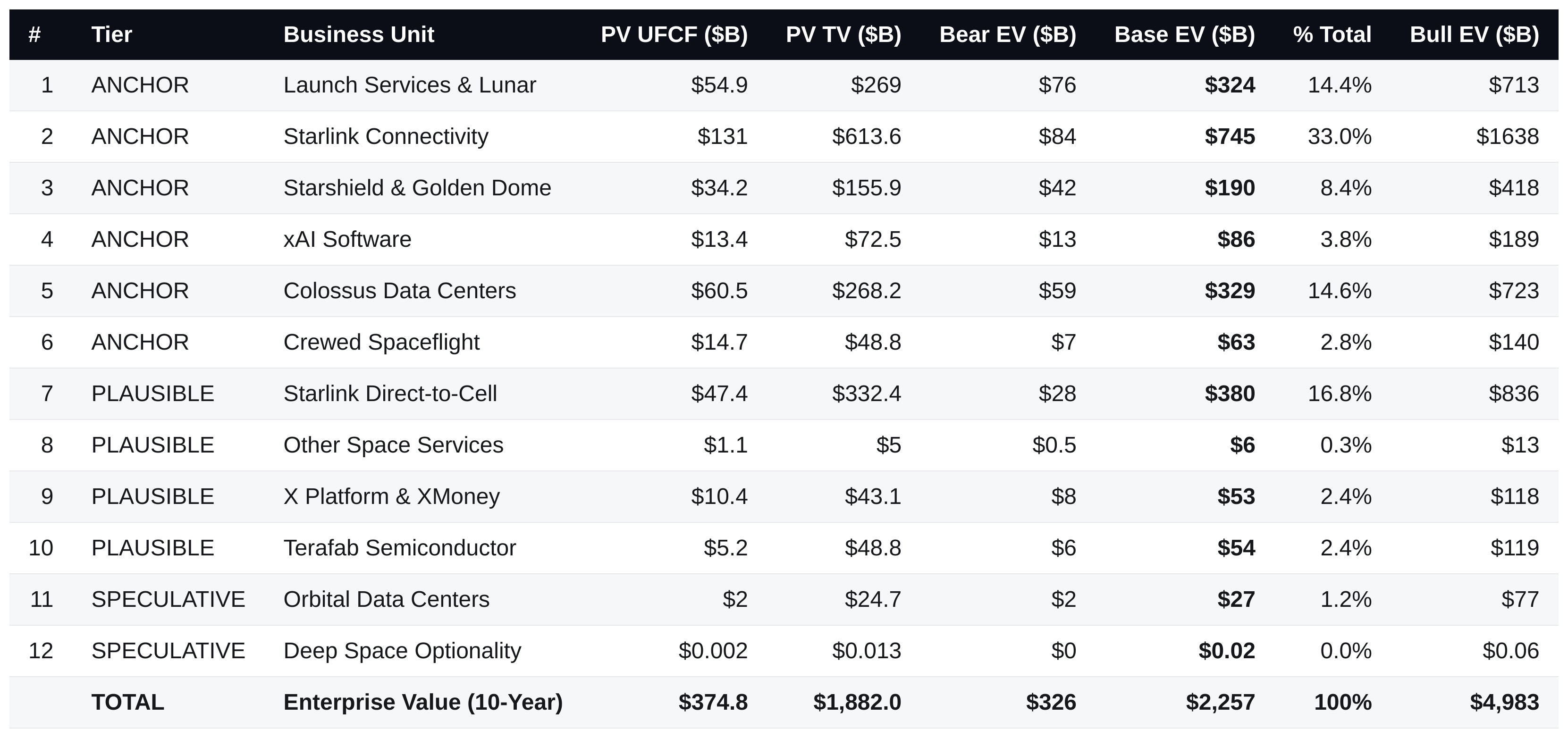

ANNEX B | SUM-OF-THE-PARTS VALUATION

B

Sum-of-the-Parts Valuation

Per-segment PV of 10-year UFCF + Gordon Growth terminal value. WACC 9.0%, terminal g 4.0%.

WACC 9.0% | Terminal g 4.0% | PV UFCF = SUMPRODUCT of 10yr UFCF with discount factors | PV TV = Gordon Growth on year-10 UFCF.

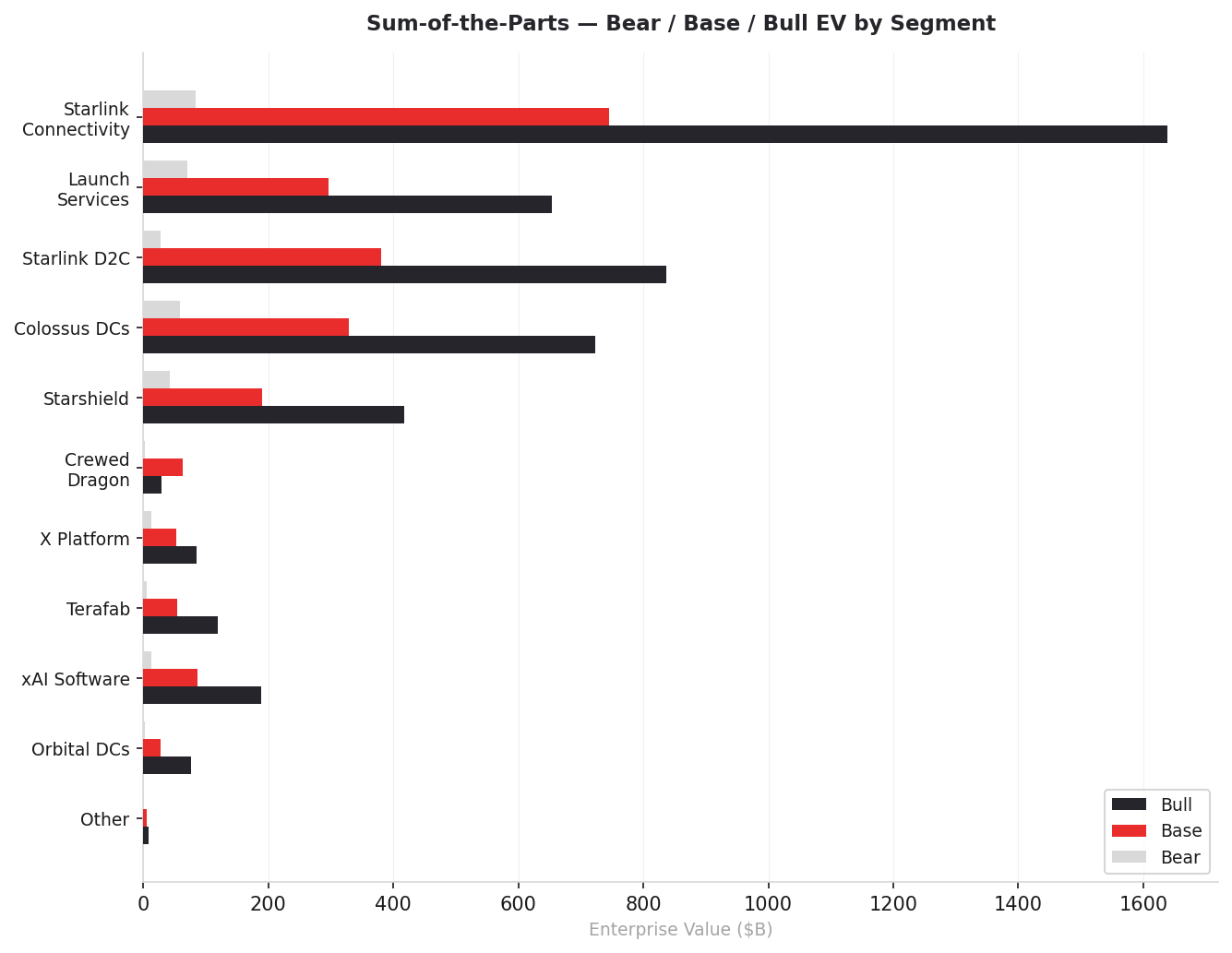

Figure B1: SOTP enterprise value by segment. Bear / Base / Bull shown. Starlink Connectivity and Starlink Direct-to-Cell are the two largest contributors at 33.0% and 16.8% respectively.

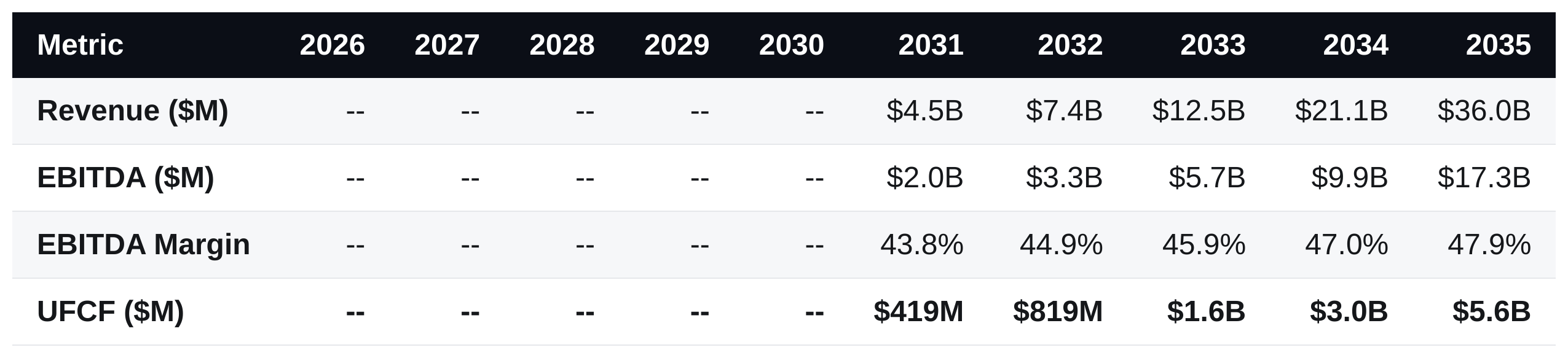

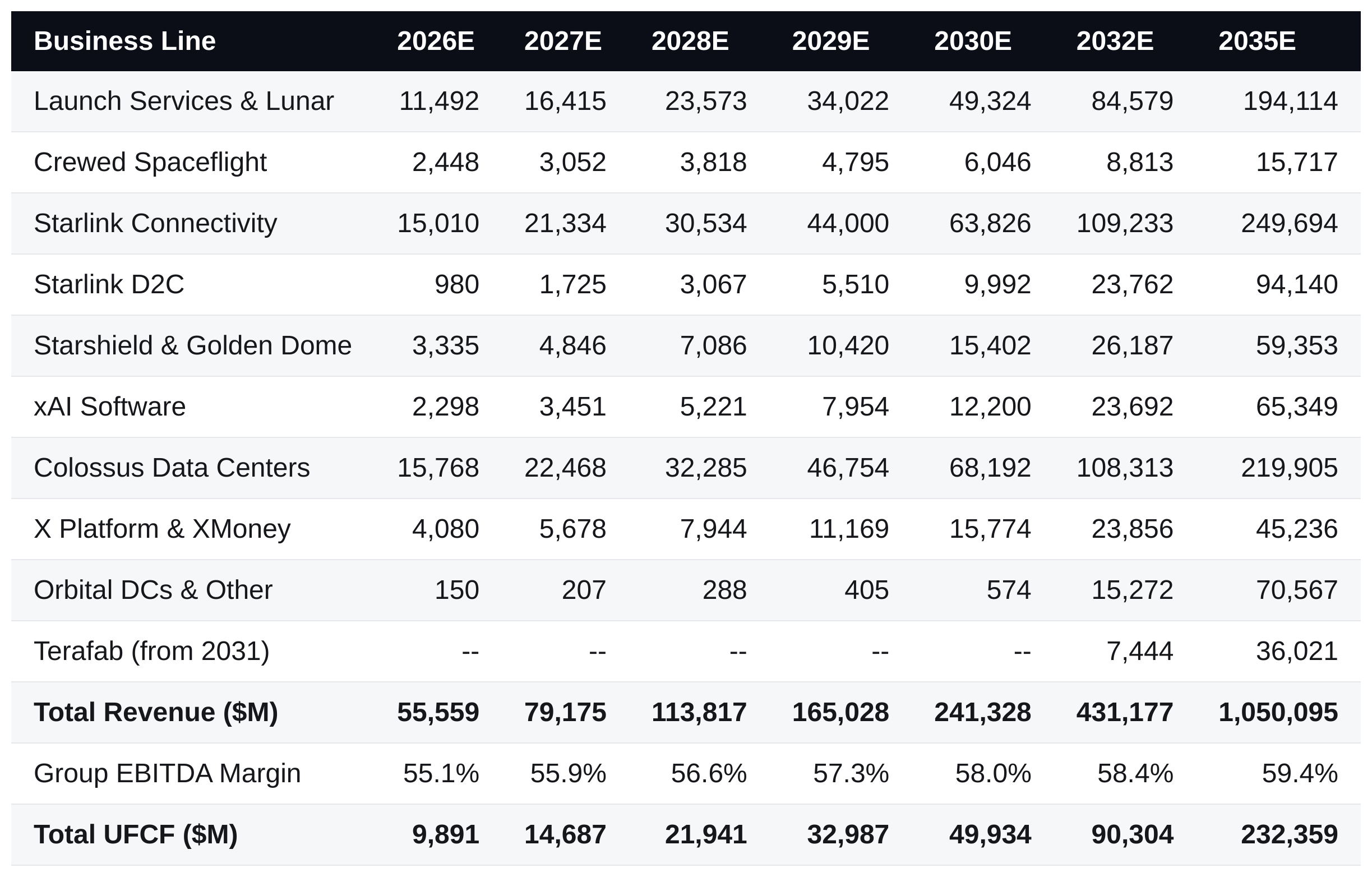

ANNEX C | CONSOLIDATED REVENUE & UFCF PROJECTIONS

C

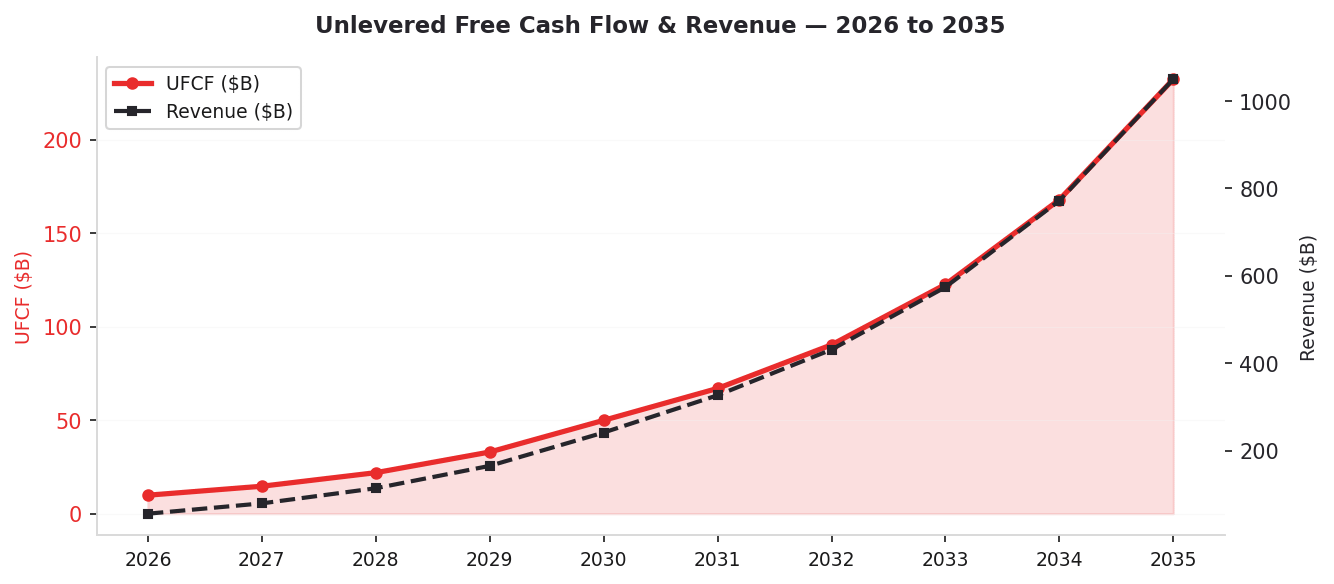

Consolidated Revenue & UFCF Projections

Probability-weighted consolidated P&L by business unit, 2026-2035. All figures in $M.

Revenue CAGR 2026-2035: ~34%. UFCF CAGR: ~37%.

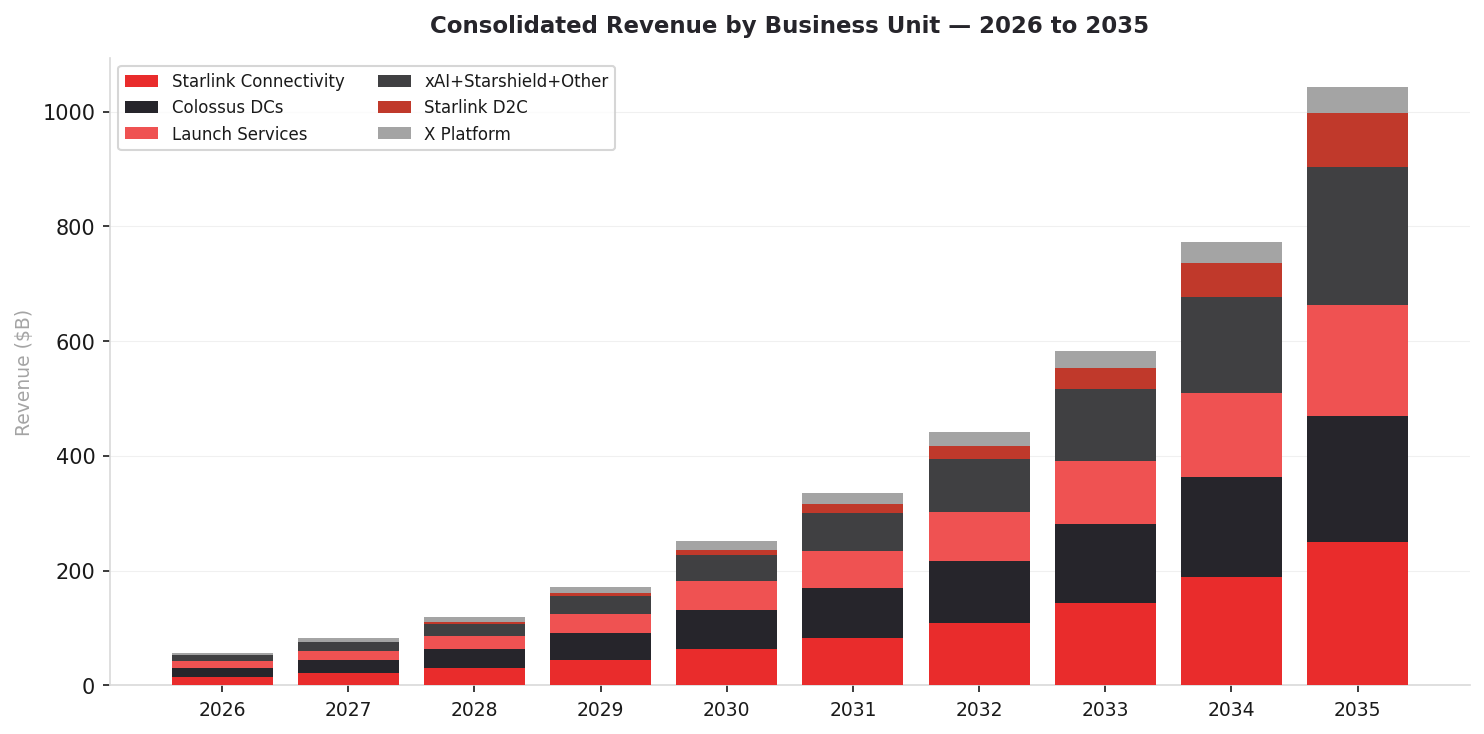

Figure C1: Consolidated revenue by business unit, stacked 2026-2035.

Figure C2: UFCF (red, left axis) and total revenue (dark, right axis) 2026-2035.

DCF Build by Horizon

ANNEX D | COMPARABLE COMPANIES ANALYSIS

D

Comparable Companies Analysis

Trading multiples. SpaceX 2026E: revenue $55.6B, EBITDA $30.6B.

Figure D1: EV/Revenue multiples. SpaceX at DCF conclusion (43.5x) shown in red.

ANNEX E | ELON PREMIUM & IMPLIED VALUATION METHODS

E

Elon Premium & Implied Valuation Methods

Peer-multiple implied valuations applied to SpaceX 2026E financials ($55.6B revenue, $30.6B EBITDA).

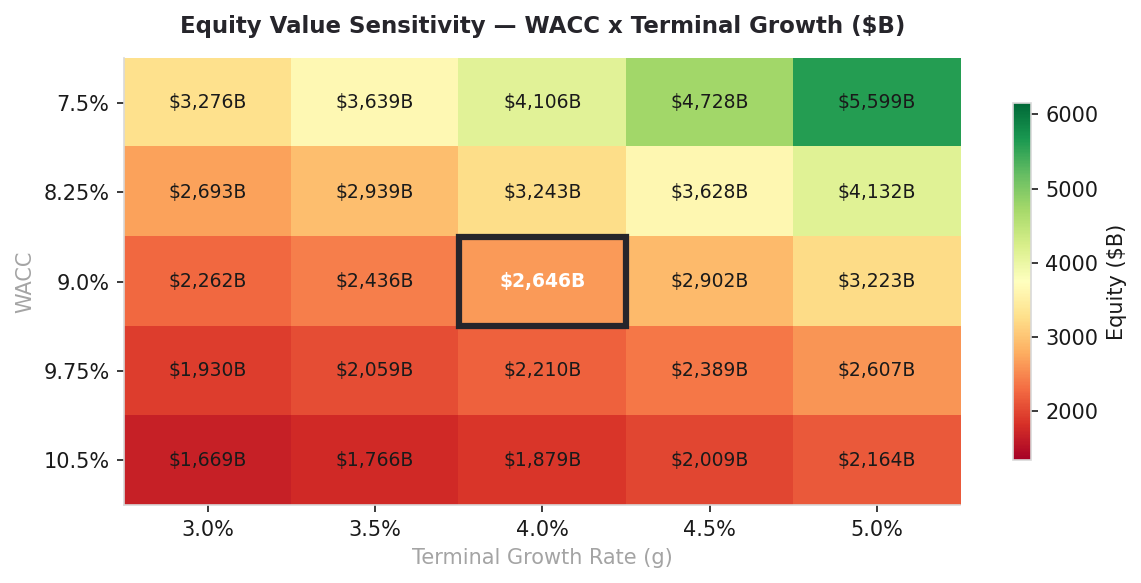

ANNEX F | SENSITIVITY & SCENARIO ANALYSIS

F

Sensitivity & Scenario Analysis

WACC x terminal growth grid and sensitivity tornado. Base: WACC 9.0%, g 4.0%, EV $2,421B, equity $2,408B.

Table F1 -- Blended Enterprise Value ($B): WACC x Terminal Growth Rate

Table F2 -- Value per Share ($): WACC x Terminal Growth Rate

Figure F1: Equity value heat map. Base case (WACC 9.0%, g 4.0%) outlined in dark.

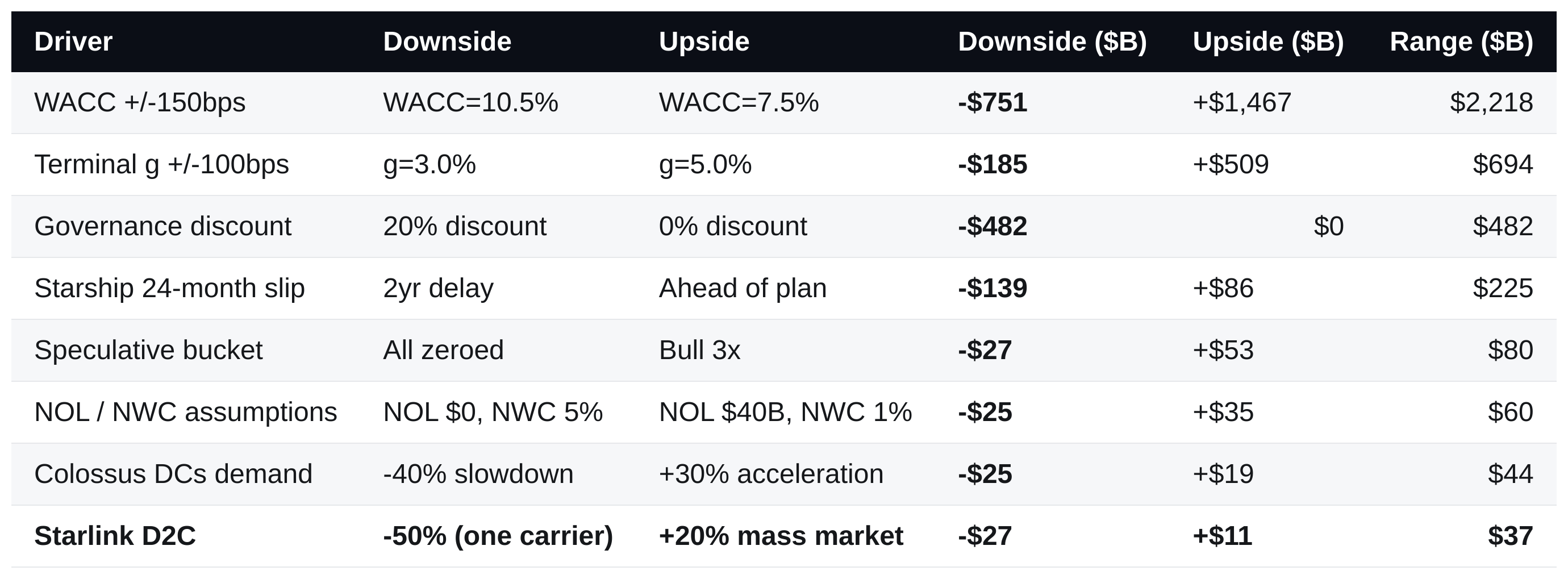

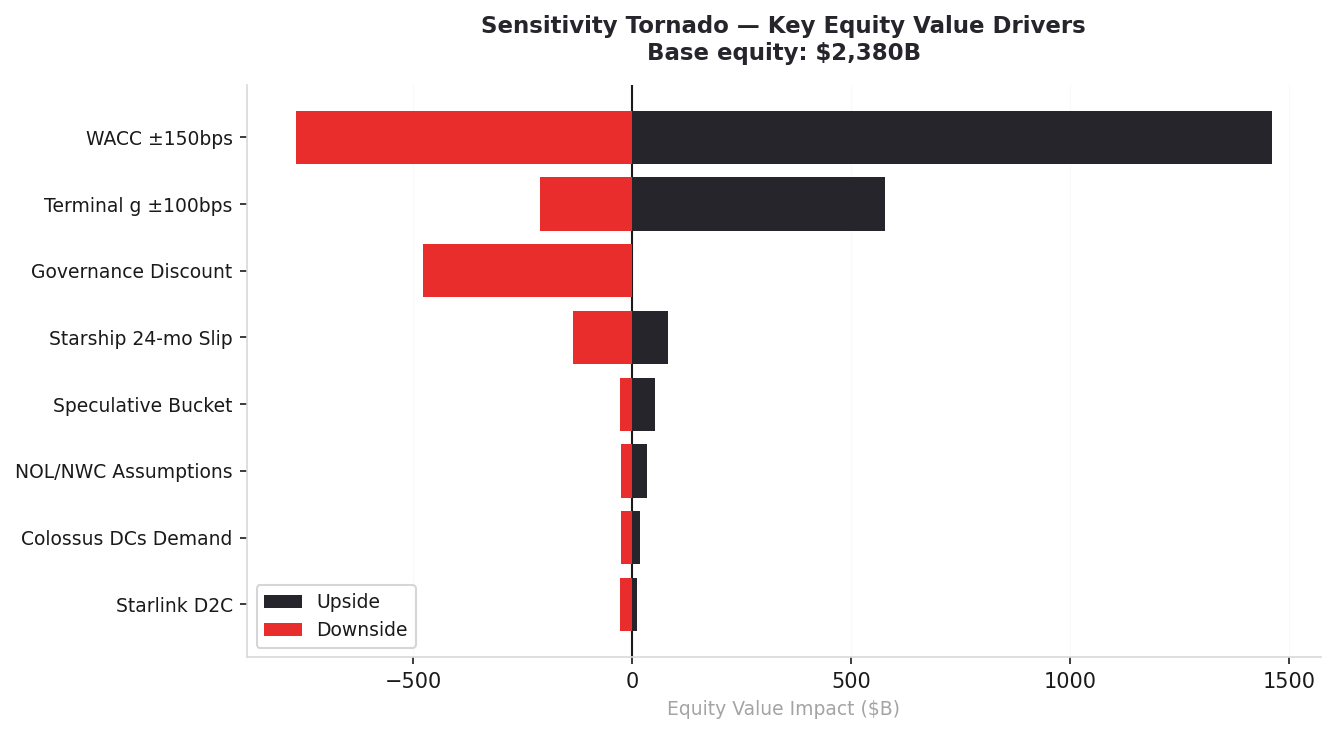

Table F3 -- Sensitivity Tornado

Figure F2: Sensitivity tornado. Drivers sorted by range. WACC and governance discount are the dominant risks.

ANNEX G | BUSINESS UNIT DETAIL -- REVENUE, EBITDA & FCF

G

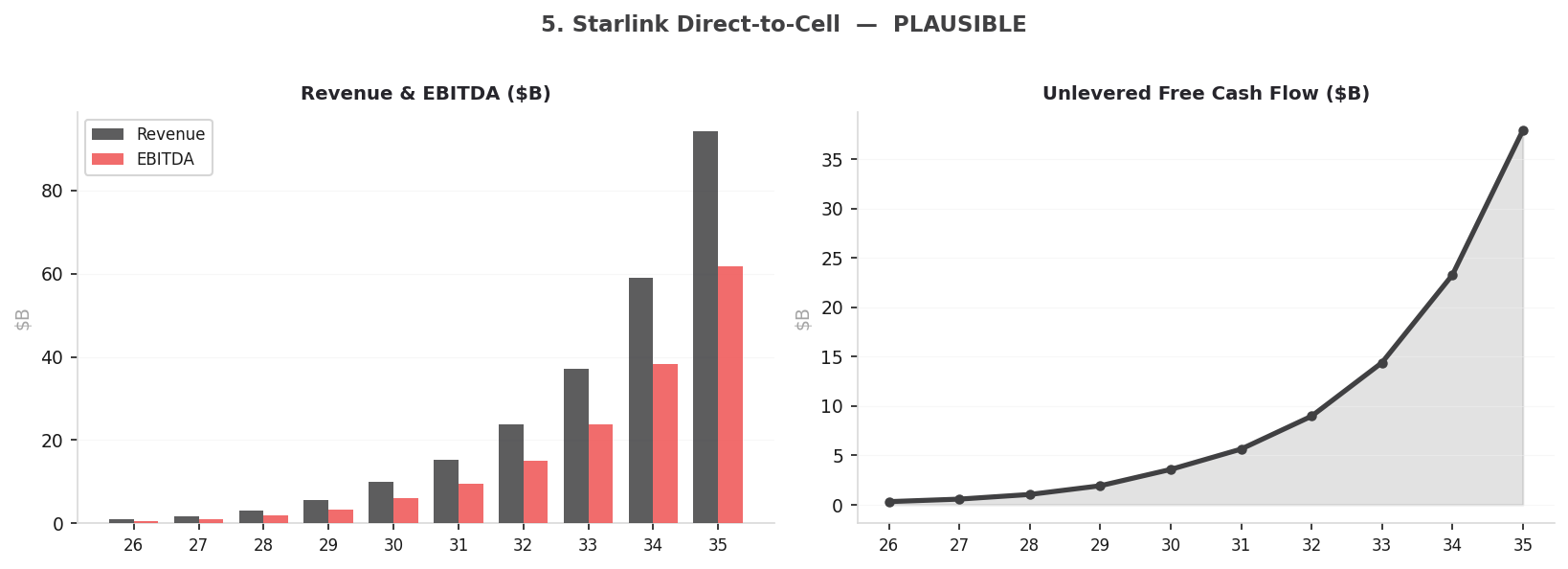

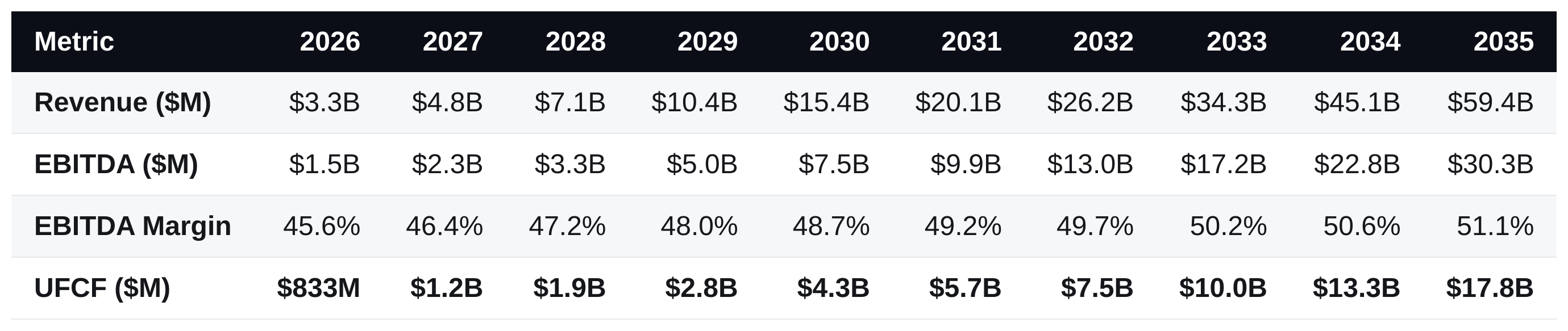

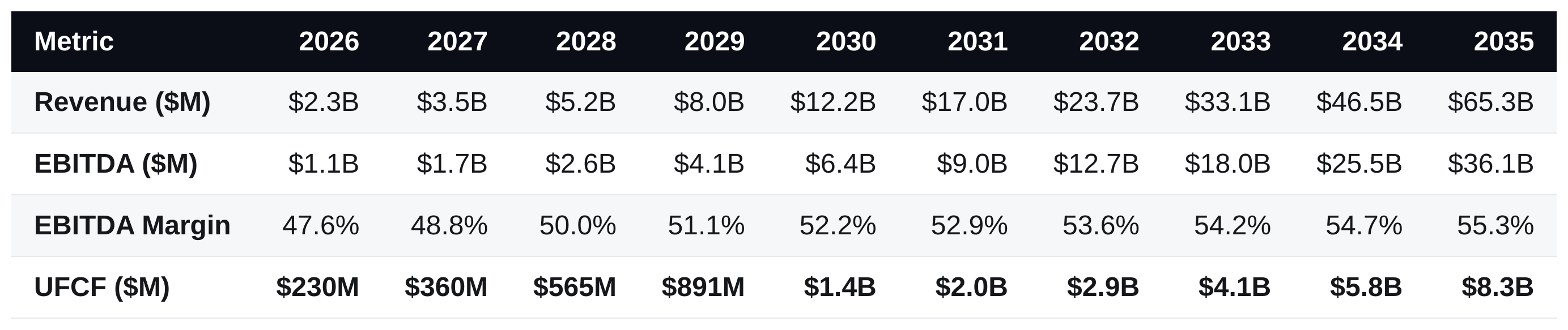

Business Unit Detail -- Revenue, EBITDA & FCF

Probability-weighted revenue, EBITDA, and UFCF for each of the 12 segments, 2026-2035.

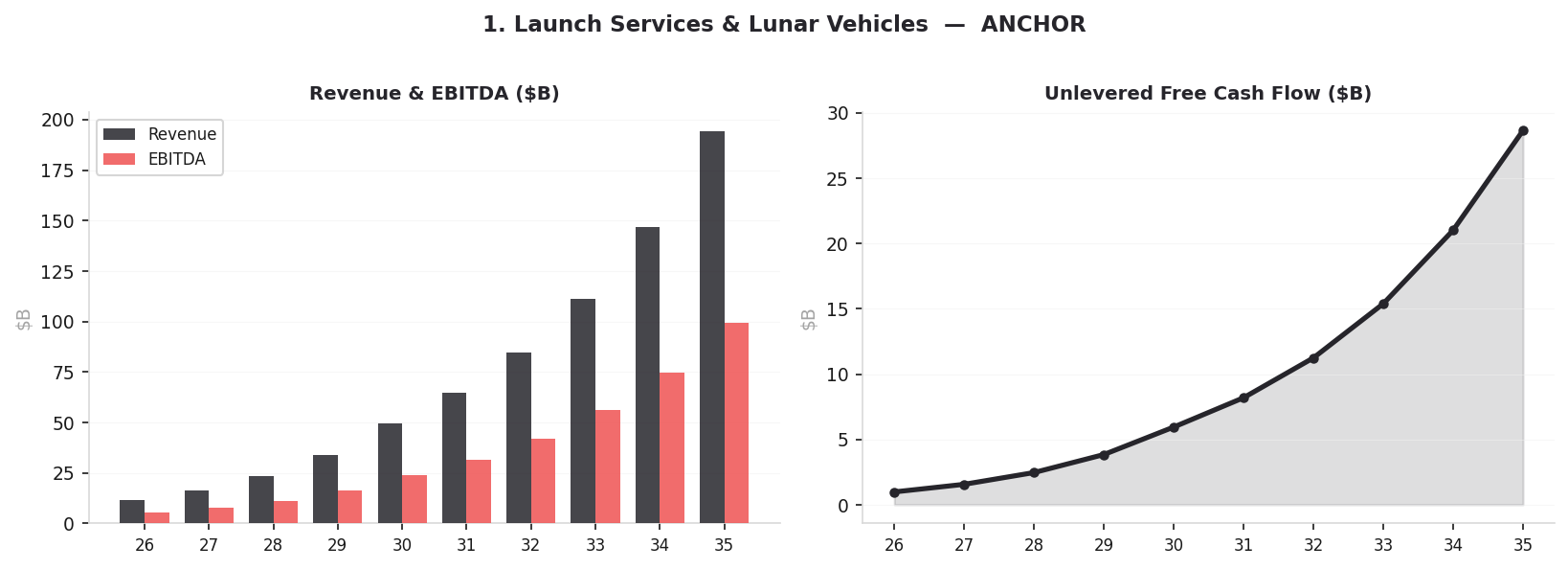

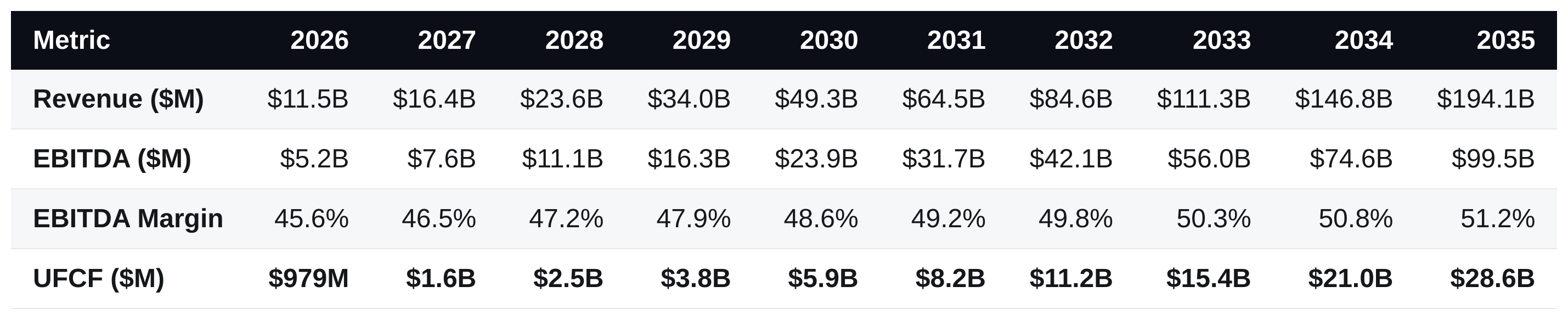

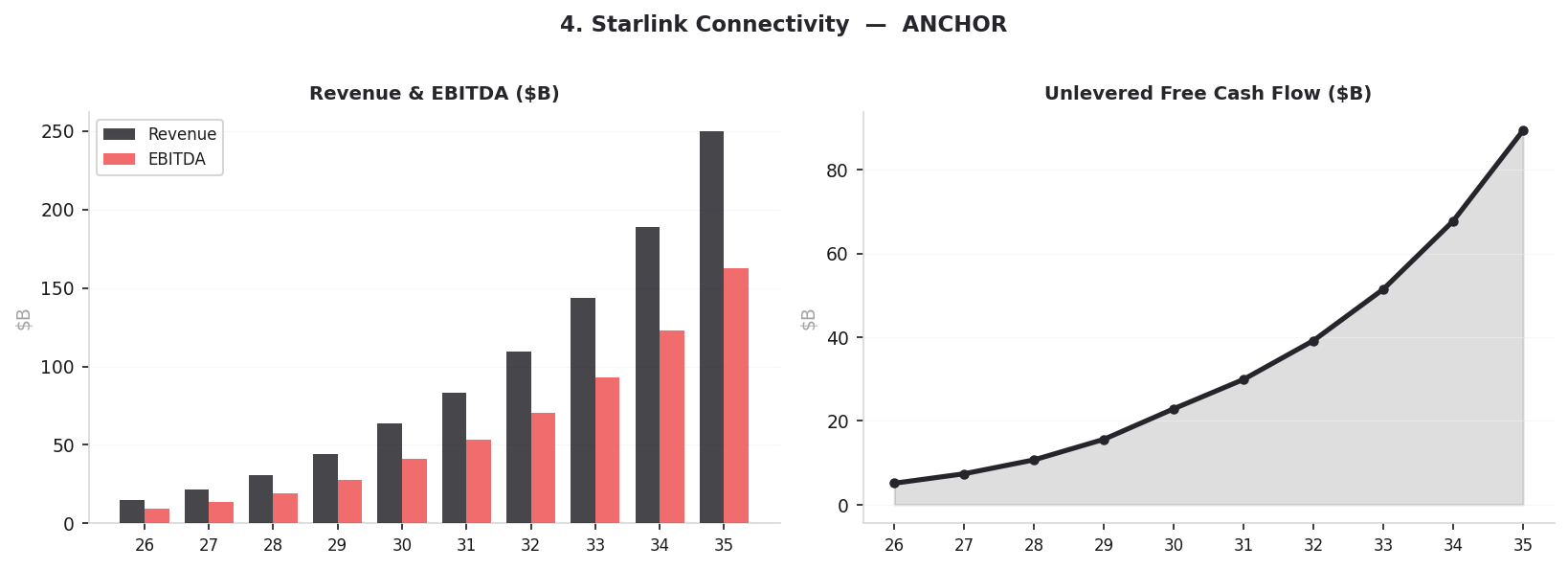

1 | ANCHOR | Base EV $324B

Launch Services & Lunar Vehicles

Falcon 9/Heavy commercial + Starship cargo ramp. S-1 Space segment 2025: $4.1B. CAGR 2026-2035: ~33%.

Figure G1: Revenue & EBITDA (left), UFCF (right), 2026-2035.

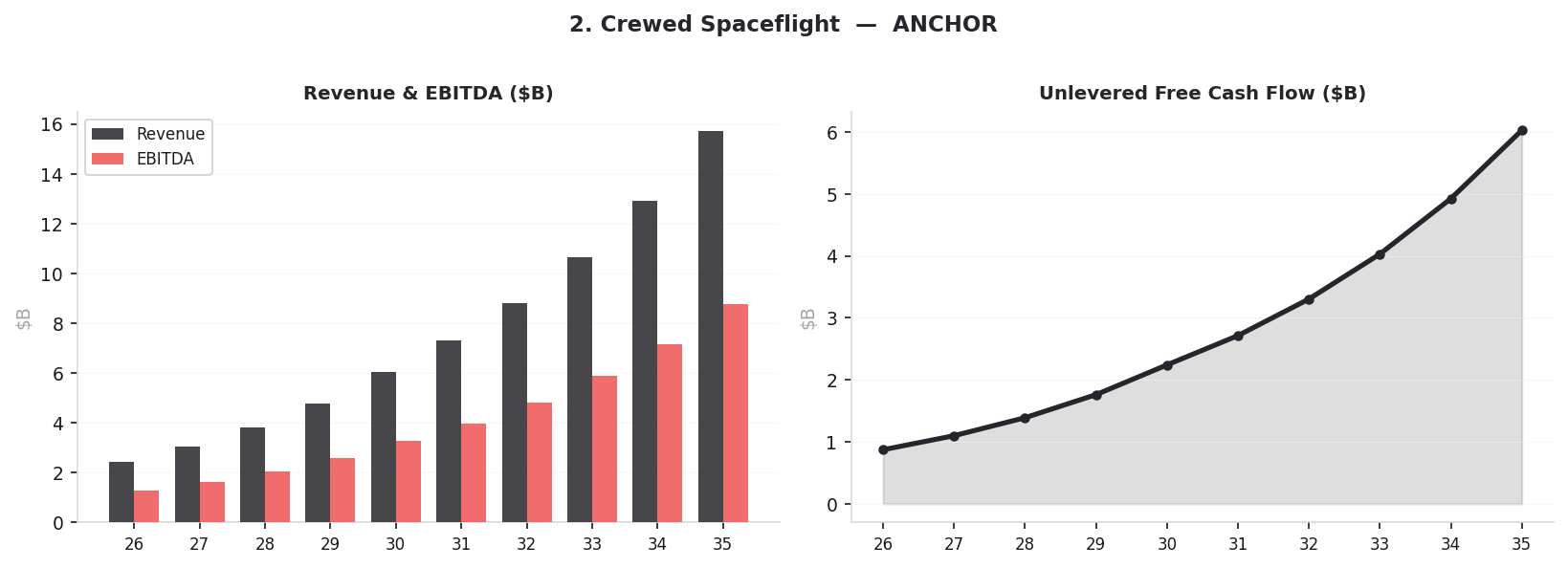

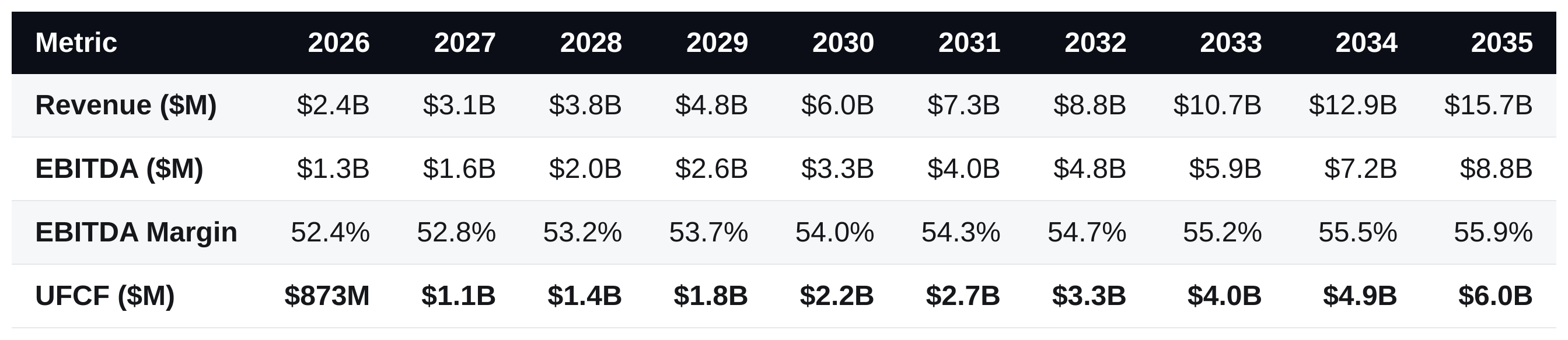

2 | ANCHOR | Base EV $63B

Crewed Spaceflight

NASA CCP/CRS Dragon + Axiom, Polaris, private spaceflight. CAGR 2026-2035: ~23%.

Figure G2: Revenue & EBITDA (left), UFCF (right), 2026-2035.

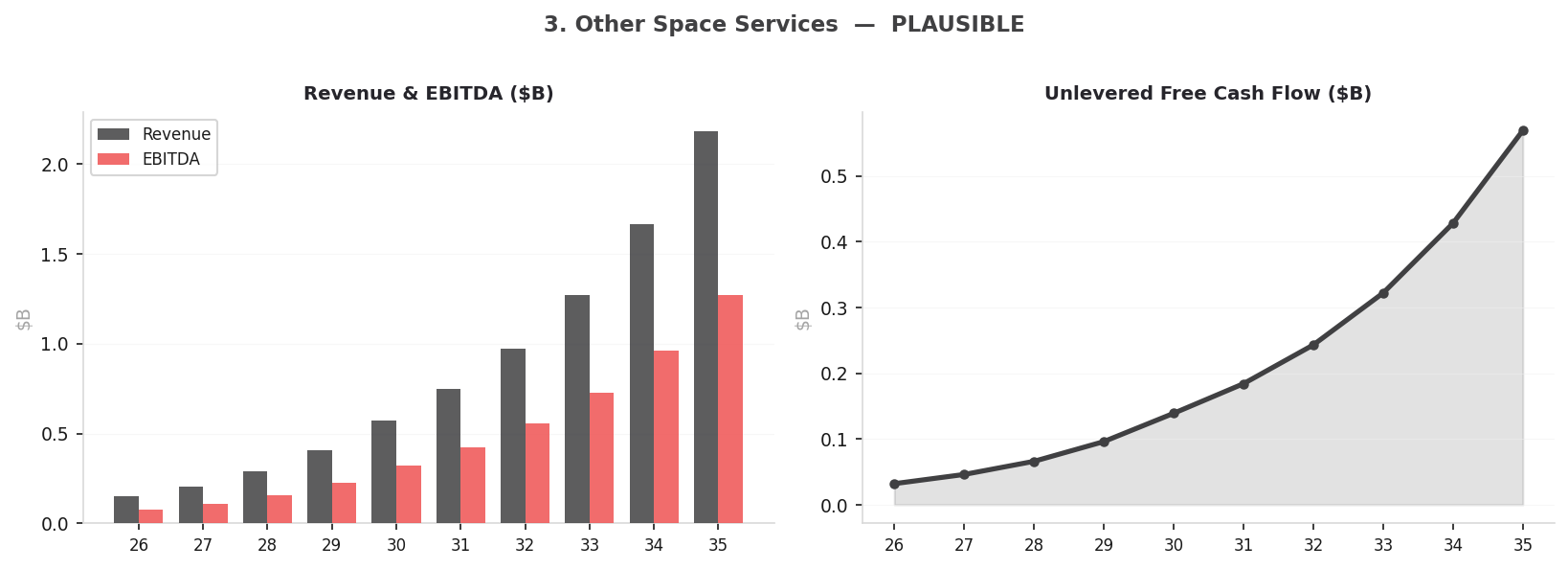

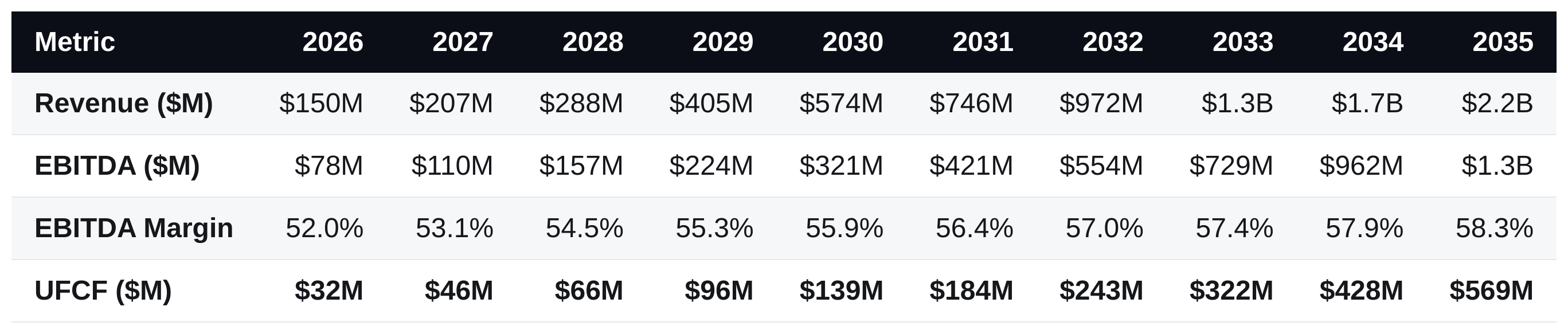

3 | PLAUSIBLE | Base EV $6B

Other Space Services

Satellite servicing, orbital tug, rocketry IP licensing. CAGR 2026-2035: ~31%.

Figure G3: Revenue & EBITDA (left), UFCF (right), 2026-2035.

4 | ANCHOR | Base EV $745B

Starlink Connectivity

10M+ subscribers, 164 countries. S-1 2025: $11.4B, 62.9% EBITDA margin. CAGR 2026-2035: ~32%.

Figure G4: Revenue & EBITDA (left), UFCF (right), 2026-2035.

5 | PLAUSIBLE | Base EV $380B

Starlink Direct-to-Cell

~300 DTC satellites. T-Mobile, KDDI, Optus, Rogers. CAGR 2026-2035: ~62%.

Figure G5: Revenue & EBITDA (left), UFCF (right), 2026-2035.

6 | ANCHOR | Base EV $190B

Starshield & Golden Dome

$6.45B in new Golden Dome contracts in 2026. NRO + PLEO IDIQ $13B ceiling. CAGR 2026-2035: ~35%.

Figure G6: Revenue & EBITDA (left), UFCF (right), 2026-2035.

7 | ANCHOR | Base EV $86B

xAI Software (Grok + API)

Top-3 foundation model. Maximally truth-seeking. Cursor ~$60B acquisition likely. CAGR 2026-2035: ~40%.

Figure G7: Revenue & EBITDA (left), UFCF (right), 2026-2035.

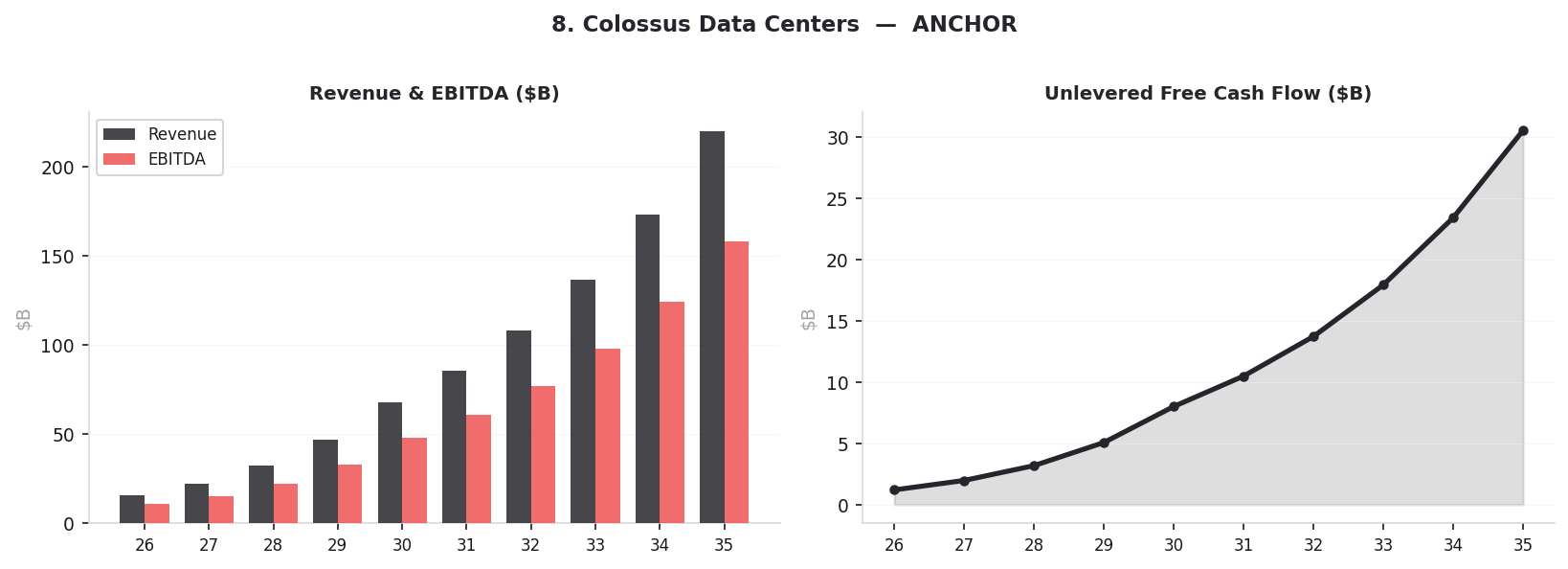

8 | ANCHOR | Base EV $329B

Colossus Data Centers

220,000 NVIDIA GPUs. $15B Anthropic agreement. 1M GPU-equivalent additions/year. CAGR 2026-2035: ~30%.

Figure G8: Revenue & EBITDA (left), UFCF (right), 2026-2035.

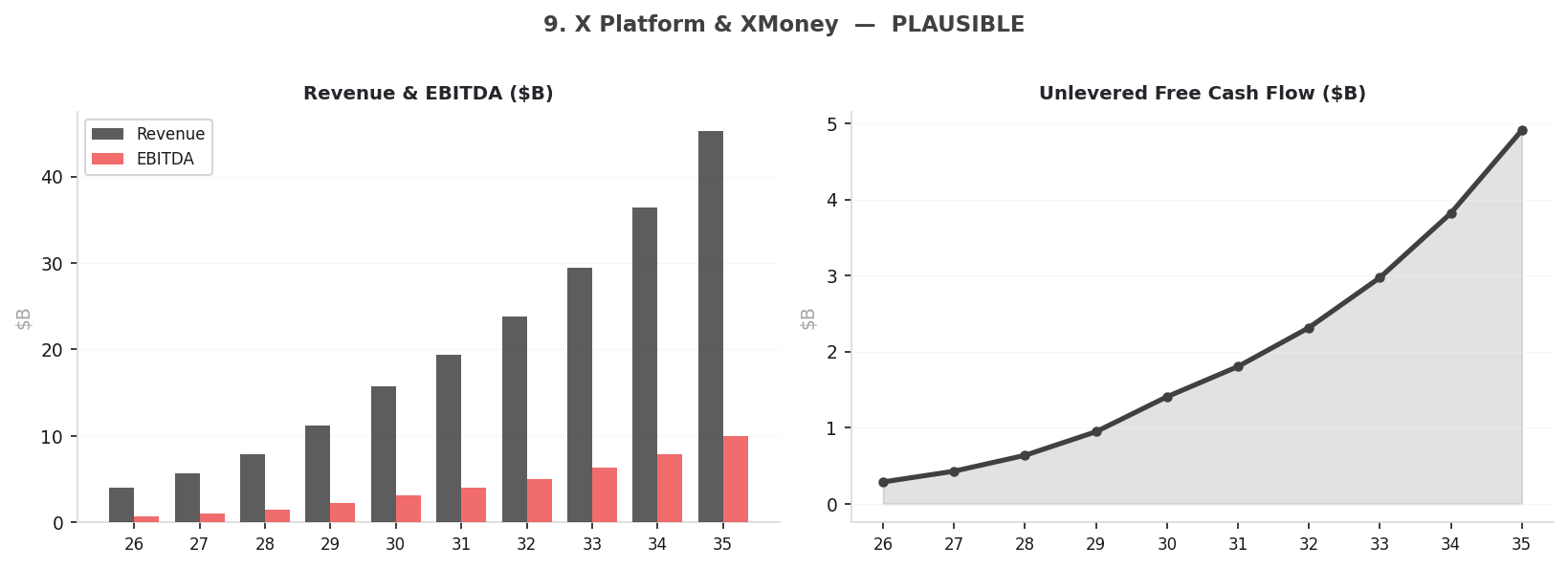

9 | PLAUSIBLE | Base EV $53B

X Platform & XMoney

600M+ MAU. XMoney: Visa, 41 states, 6% APY. 2026 base: $4.1B. CAGR 2026-2035: ~27%.

Figure G9: Revenue & EBITDA (left), UFCF (right), 2026-2035.

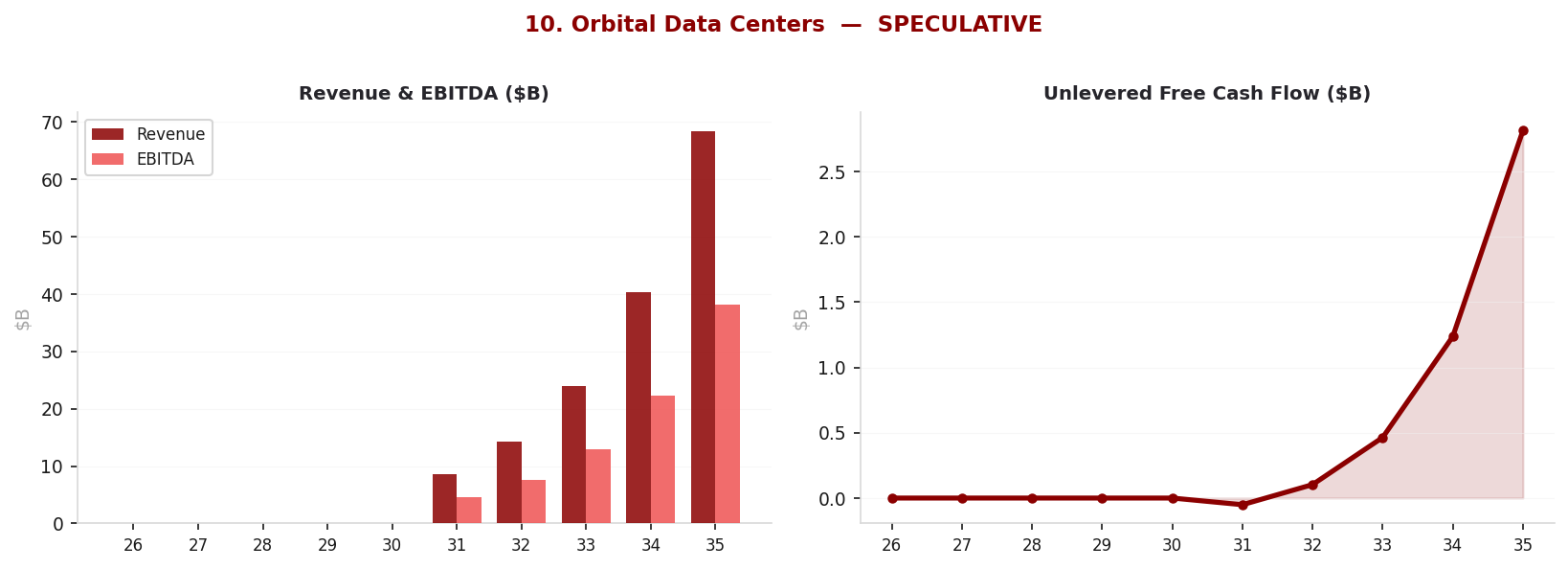

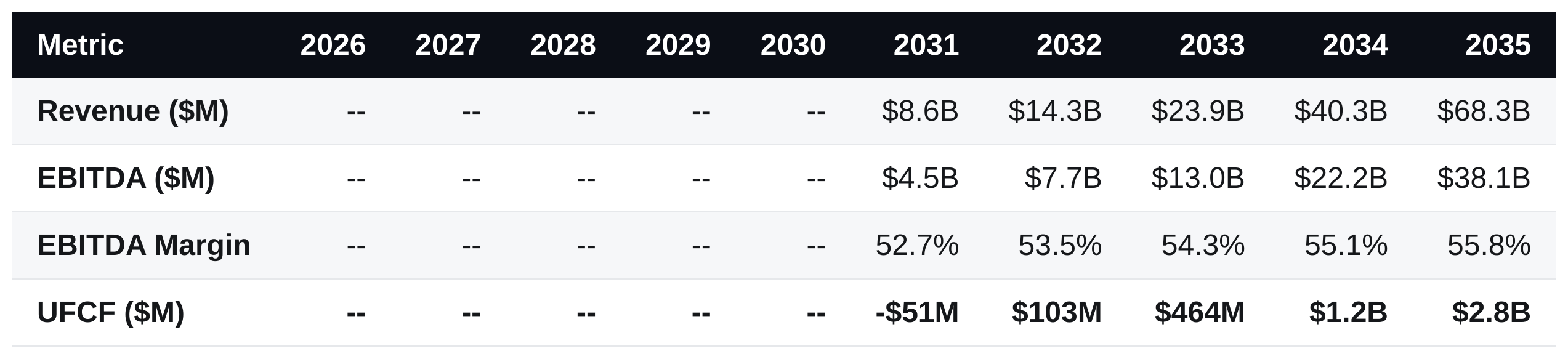

10 | SPECULATIVE | Base EV $27B

Orbital Data Centers

In-space compute: perpetual solar, deep-space radiative cooling, no NIMBY. First commercial 2031.

Figure G10: Revenue & EBITDA (left), UFCF (right), 2026-2035.

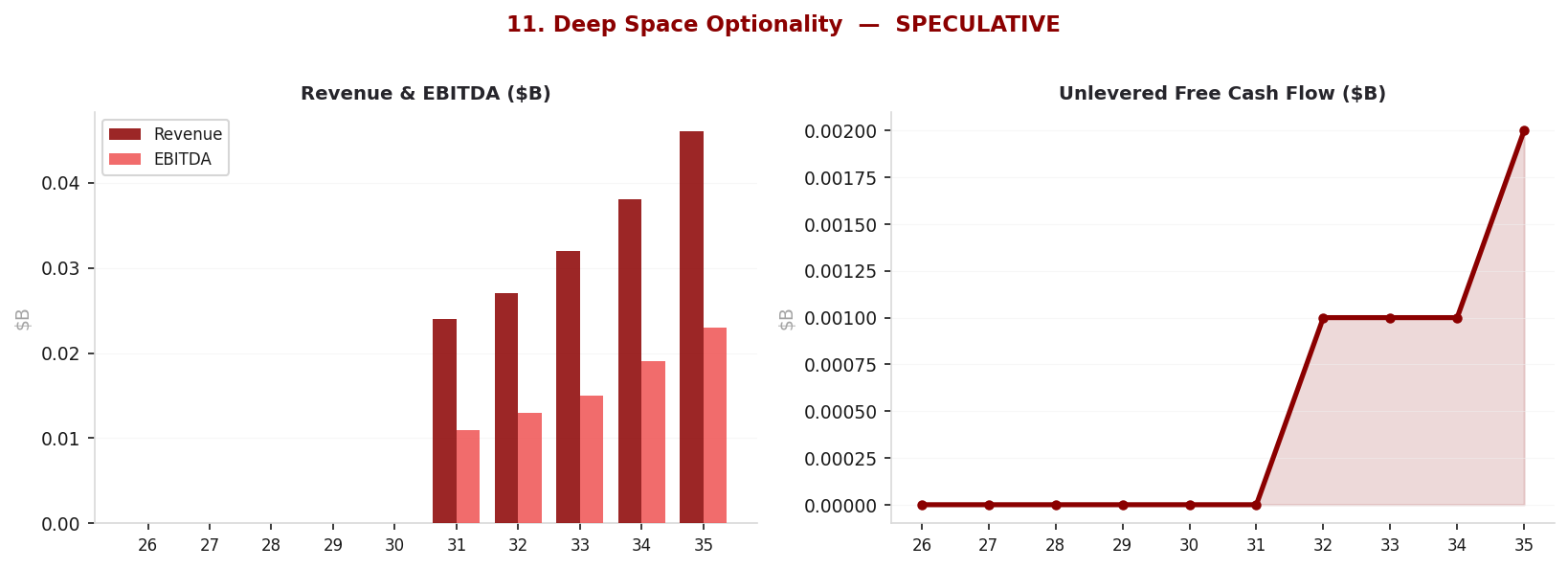

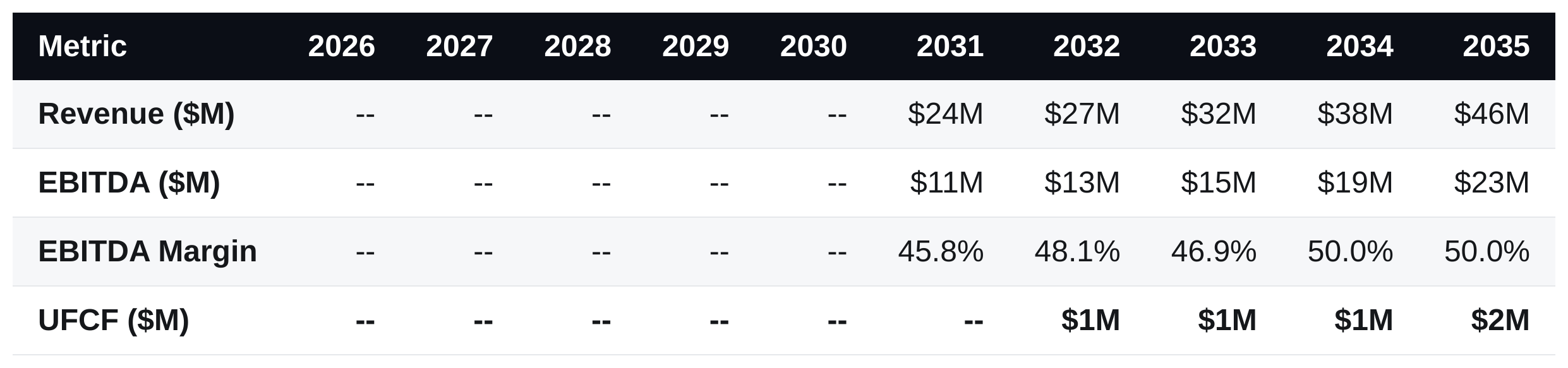

11 | SPECULATIVE | Base EV $0.02B

Deep Space Optionality

Moon/Mars cargo 2028, asteroid extraction, P2P transport. Narrative premium and talent magnet.

Figure G11: Revenue & EBITDA (left), UFCF (right), 2026-2035.

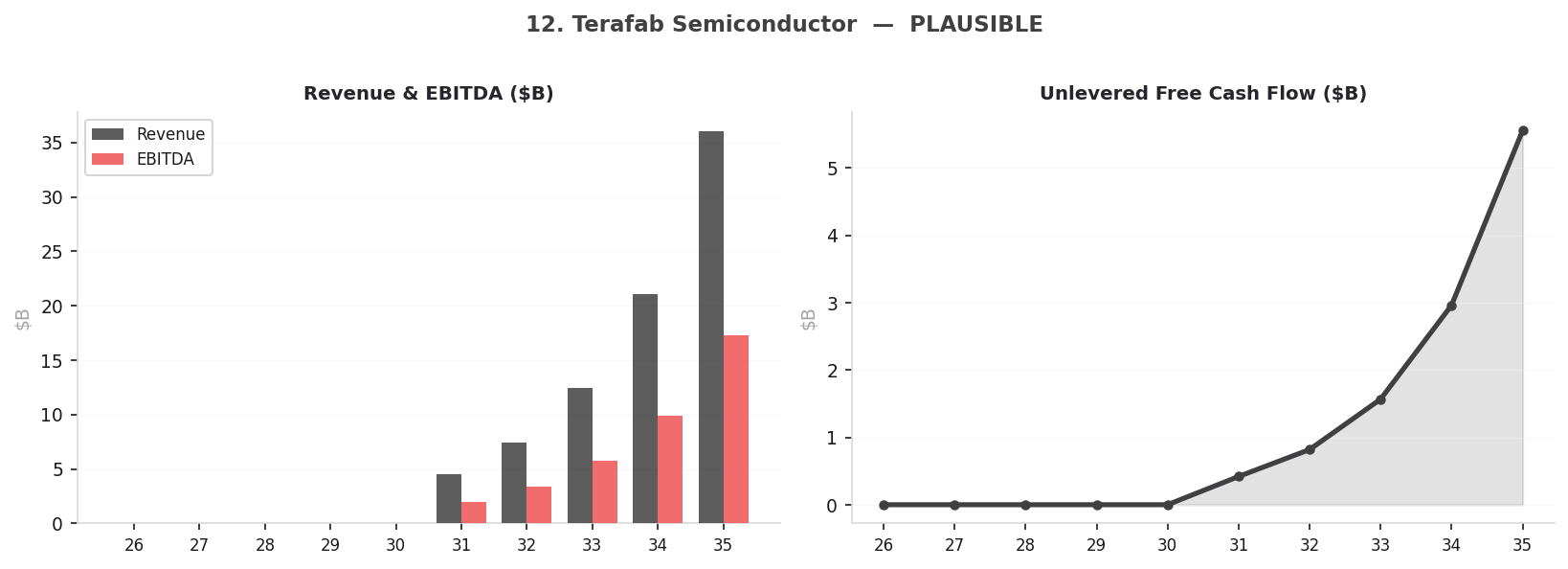

12 | PLAUSIBLE | Base EV $54B

Terafab -- Semiconductor Mfg

World largest chip fab. AI5/AI6 + D3. $55B first phase. Revenue modelled from 2031.

Figure G12: Revenue & EBITDA (left), UFCF (right), 2026-2035.